Debt collectors don’t just call—they often report debts to credit bureaus. But there are strict rules governing what they can report and how they must do it.

Understanding these rules can help you protect your credit and identify violations.

Can Debt Collectors Report to Credit Bureaus?

Yes. Debt collectors can report debts to:

- Experian

- Equifax

- TransUnion

However, the information must be:

- Accurate

- Complete

- Not misleading

FDCPA + FCRA: How They Work Together

While the FDCPA governs collection behavior, the Fair Credit Reporting Act (FCRA) regulates credit reporting.

Together, they prohibit:

- Reporting false information

- Failing to update inaccurate data

- Reporting debts not owed

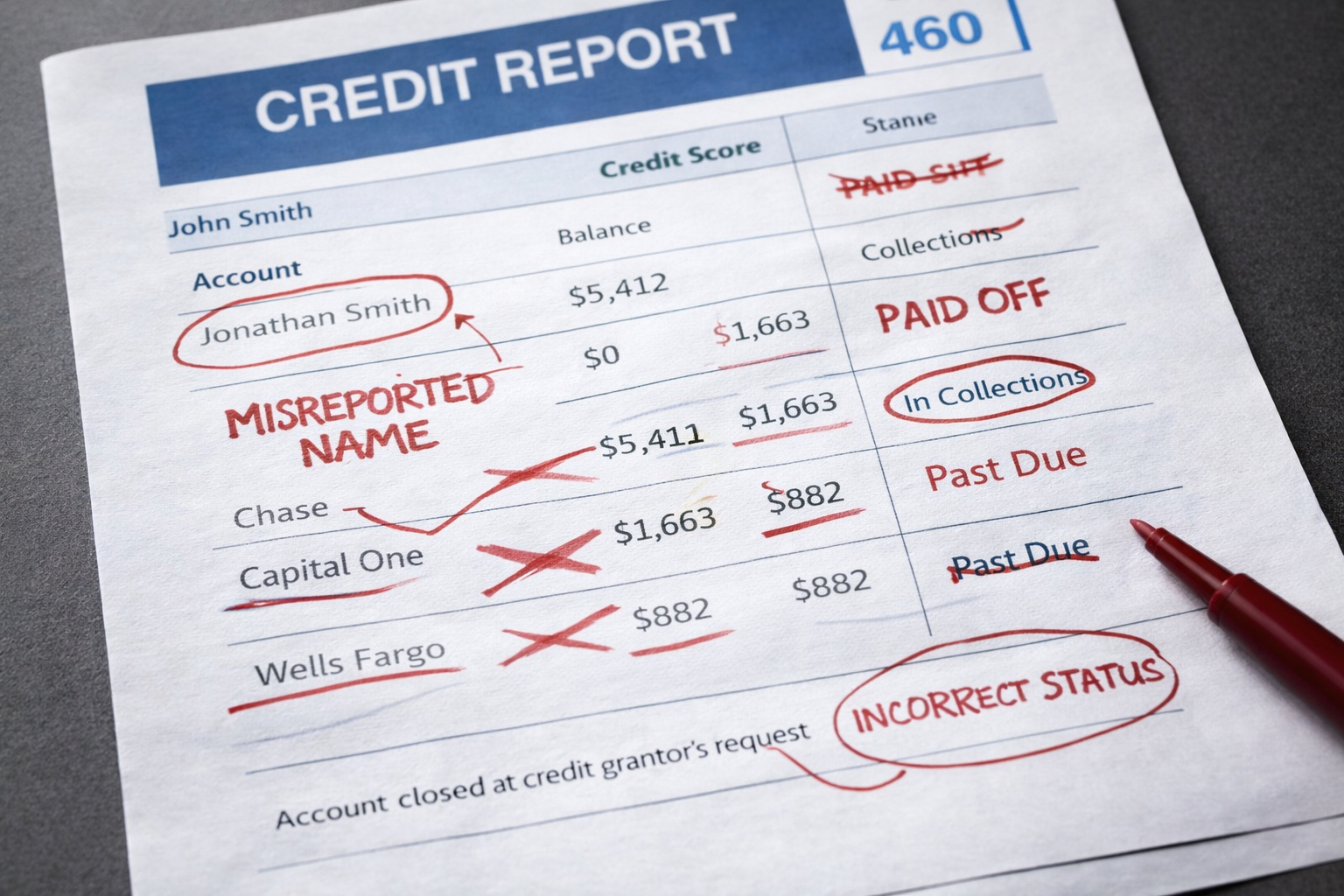

Common Credit Reporting Violations

Reporting Incorrect Amounts

Inflated balances or unauthorized fees

Reporting the Wrong Person

Mixing up identities or accounts

Failing to Mark Debt as Disputed

If you dispute a debt, it must be noted

Re-Aging Debt

Changing dates to make old debt appear new

What Happens If You Dispute a Debt?

When you dispute:

- The collector must investigate

- They must report the dispute

- They must correct inaccuracies

Can a Collector Report Without Contacting You?

Yes—but they must still comply with validation and accuracy requirements.

How Credit Reporting Affects You

Negative reporting can:

- Lower your credit score

- Affect loan approvals

- Increase interest rates

How to Protect Yourself

- Monitor your credit reports regularly

- Dispute inaccurate information

- Keep documentation of all communications

What If a Collector Reports Incorrect Information?

If false information is reported:

- Dispute with the credit bureau

- Notify the collector

- Contact an attorney

What Damages Can You Recover?

If your rights are violated, you may recover:

- Statutory damages

- Actual damages

- Attorney’s fees

Final Thoughts

Debt collectors have the power to impact your credit—but they must follow strict rules. When they don’t, you have the right to fight back.

If you notice errors or unfair reporting, taking action quickly can protect your credit and potentially lead to compensation.