You’ve worked hard to pay your bills on time. You’ve balanced your budget, skipped the extra latte, and played by the rules. Then, you go to apply for a mortgage or a car loan, and the officer gives you “the look.”

The “Your-Credit-Score-is-Trash” look.

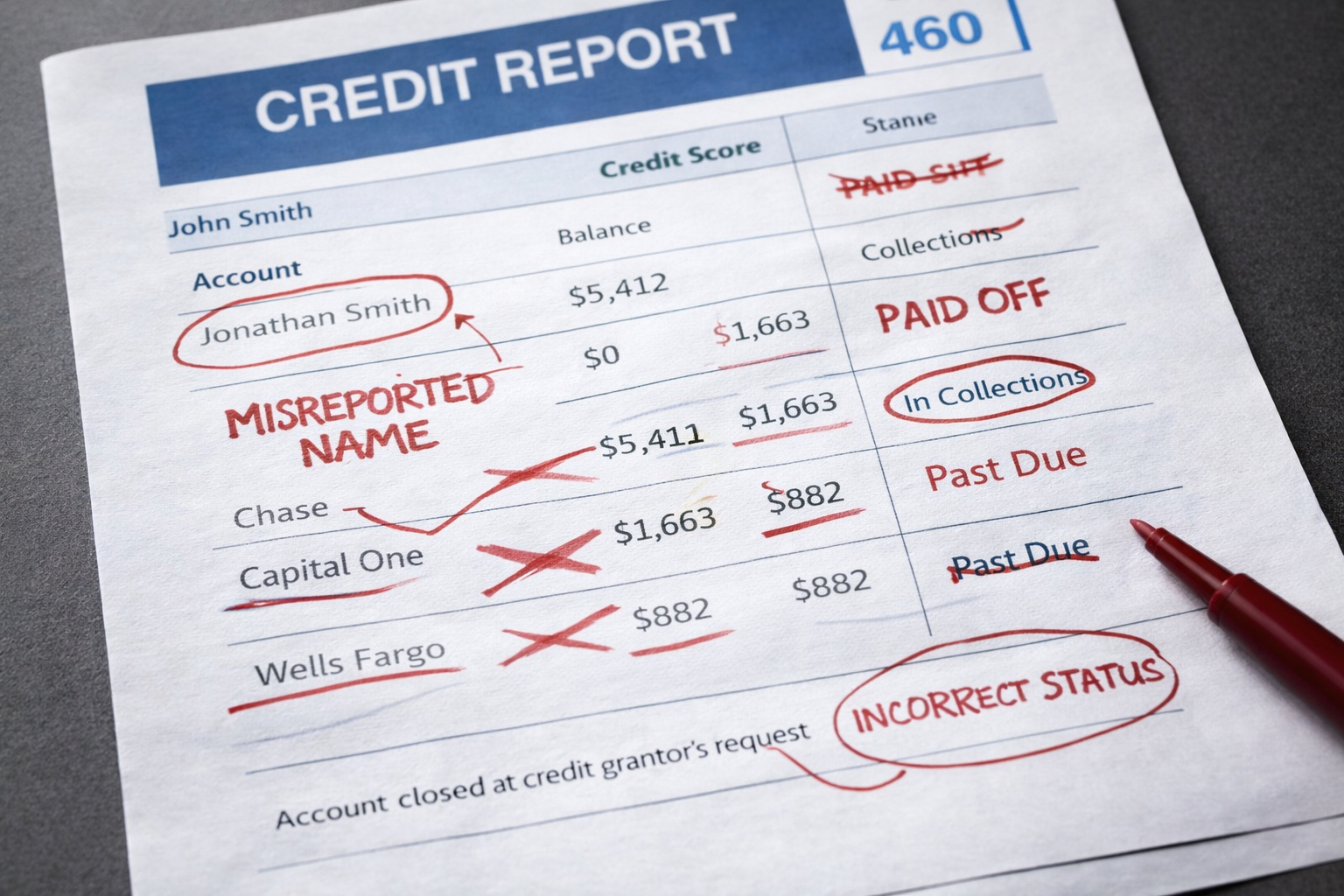

You check your report and see a collection account you don’t recognize, a late payment from five years ago that never happened, or, even worse, someone else’s debt entirely. You try to dispute it, but the credit bureaus send back a generic letter saying the information has been “verified.”

This is where most people give up. This is also where a credit report error attorney becomes your secret weapon.

Getting legal help for credit errors isn’t just about “fixing a number.” It’s about holding multi-billion dollar corporations accountable for the mess they’ve made of your life.

The Rule: Your Rights Under the Fair Credit Reporting Act (FCRA)

The Fair Credit Reporting Act (FCRA) is a federal law that was built specifically to protect you. It’s the rulebook that credit bureaus (Equifax, Experian, and TransUnion) and the companies reporting to them (furnishers) must follow.

Under the FCRA, you have three primary rights regarding your data:

- Accuracy: Every piece of information on your report must be accurate.

- Completeness: Your report shouldn’t leave out key details that make a record look worse than it is.

- Verifiability: If a bureau cannot prove the information is yours and accurate, they must remove it.

⚠️ The Reality Check: While the law says they must fix it, they often don’t. Credit bureaus process millions of disputes using automated systems. They aren’t looking for the truth; they are looking to close a ticket.

👉 The Bottom Line: If a bureau fails to conduct a “reasonable investigation” after you’ve disputed an error, they have violated the law. And when they violate the law, you can sue them.

Why “Doing It Yourself” Often Hits a Brick Wall

Many consumers start by using the online dispute portals provided by the bureaus. Don’t do this.

Online portals often force you to choose from a limited “menu” of reasons for your dispute. This restricts your ability to provide a full narrative and attach complex evidence. Even worse, some portals include fine print that may waive your right to a jury trial in favor of arbitration.

When you send a DIY letter, the bureau’s computer system “summarizes” your multi-page explanation into a two-digit code. That code is what the creditor sees. The nuance of your situation is lost in translation.

The Bureau’s “Verified” Response

You’ll likely receive a letter 30 days later stating: “We have investigated your dispute and the information has been verified as accurate.”

For most, this is the end of the road. For a credit report error attorney, this is just the beginning.

The Secret: Why an Attorney is Different from “Credit Repair”

There is a massive difference between a credit repair company and a credit report error attorney.

- Credit Repair Companies: These are often “mills” that send the same generic, repetitive letters to bureaus every month. They charge you a monthly fee, but they have no actual “teeth.” If the bureau says “no,” the credit repair company just sends the same letter again.

- Credit Report Error Attorneys: We are legal professionals. We don’t just “ask” the bureaus to fix it: we demand it under the threat of litigation. If they refuse to follow the FCRA, we can file a federal lawsuit.

What an Attorney Can Do That a “Service” Can’t:

- File Federal Lawsuits: We take the bureaus to court.

- Recover Money Damages: You may be entitled to “actual damages” (like the money you lost due to a higher interest rate) and “statutory damages” of up to $1,000 per violation.

- Force a Correction: A judge can order the bureau to fix your record.

- Zero Out-of-Pocket Costs: Because the FCRA has a “fee-shifting” provision, the credit bureau often has to pay our legal fees if we win. This means we can often represent you with no upfront cost.

⚠️ Common Credit Report Errors to Watch For

Not every error is as obvious as a wrong name. Some are subtle but equally damaging:

- Mixed Files: This happens when your information is merged with someone else who has a similar name or SSN.

- Re-aging Debt: When a creditor changes the date of a delinquency to make it look newer, keeping it on your report longer than the legal 7-year limit.

- Identity Theft Accounts: Accounts opened in your name without your permission.

- “Settled” vs. “Paid in Full”: Reporting a settled account as “charged off” or “unpaid.”

- Duplicate Records: Listing the same debt multiple times under different collection agency names.

Step-by-Step: How to Prepare for Your Legal Consultation

If you are ready to stop being a victim of the bureaus, you need to be organized. Follow this checklist before calling us:

- Pull Your Reports: Get a fresh copy of all three reports (Experian, Equifax, TransUnion).

- Highlight the Lies: Use a physical highlighter to mark every single inaccuracy.

- Gather the Proof: Find your cancelled checks, bank statements, or “letter of satisfaction” that proves the bureau is wrong.

- Save Your Denials: If you’ve already disputed and were rejected, keep those “verified” letters. They are evidence of the bureau’s failure to investigate.

The “Fresh Start” Is Possible

Imagine waking up and knowing your credit score actually reflects your financial responsibility. Imagine walking into a dealership and getting the best interest rate available, not the “predatory” one.

That is what a clean record provides. It provides freedom.

If you’ve tried to fix your credit and the bureaus aren’t listening, it’s time to stop talking and start suing.

Next Steps: Take Action Today

✅ Step 1: Download your credit reports from AnnualCreditReport.com.

✅ Step 2: Identify any errors that have remained after a previous dispute.

✅ Step 3: Contact a credit report error attorney for a free case evaluation.

Don’t let a computer error dictate your future. The law is on your side: you just need a team that knows how to use it.

")