(“Wait… I get to keep stuff?”)

Yes. And this is one of the most important—and most misunderstood—parts of filing bankruptcy.

When people think about bankruptcy, they often imagine losing everything. But that’s not how it works. In reality, the law is designed to give you a fresh start, not leave you with nothing.

That’s where exemptions come in.

If you’re filing bankruptcy in Pennsylvania, understanding exemptions is critical to protecting your property—and avoiding unnecessary stress.

Let’s break it down in plain English.

What Are Bankruptcy Exemptions?

At their core, exemptions are laws that allow you to keep certain property when you file bankruptcy.

Think of it like this:

- The bankruptcy system gathers your assets

- Exemptions act like a shield that protects some (or all) of those assets

Without exemptions, bankruptcy would be devastating.

With them, most people keep everything they need to live.

Pennsylvania vs. Federal Exemptions: You Have a Choice

Here’s something unique about Pennsylvania:

You can choose between Pennsylvania exemptions OR federal bankruptcy exemptions.

You don’t get to mix and match—but you do get to pick the system that works best for you.

Why does this matter?

Because Pennsylvania’s exemption system is… let’s say… not very generous.

In many cases, people filing in PA choose the federal exemptions because they offer more protection (especially for things like home equity).

But Pennsylvania exemptions still matter—and in some cases, they’re the better choice.

How Do Exemptions Actually Work?

Let’s say you own a car worth $5,000.

If there’s an exemption that protects up to $10,000 in vehicle value, your car is fully protected.

If your asset exceeds the exemption amount, things get more complicated—but often still manageable.

The key takeaway:

Exemptions don’t eliminate assets—they protect their value.

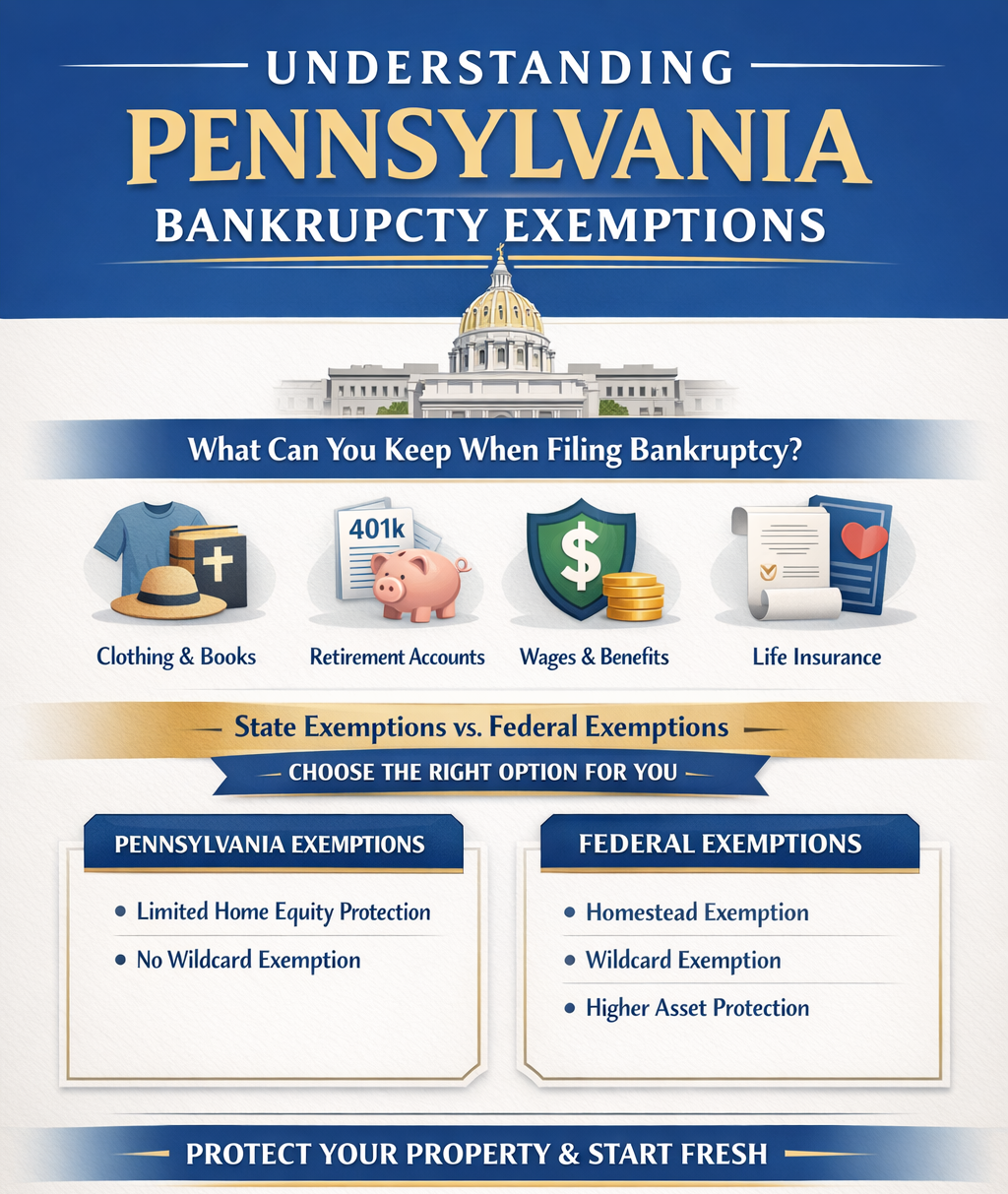

Pennsylvania Exemptions: The Basics

Pennsylvania’s exemption system is relatively limited compared to federal law, but there are still important protections.

Here are some of the key categories:

1. Clothing, Bibles, and School Books

These are fully exempt.

Which makes sense—no one is filing bankruptcy and expecting to lose their wardrobe or their kids’ textbooks.

2. Retirement Accounts

Most tax-exempt retirement accounts are protected, including:

- 401(k)s

- IRAs

- Pensions

This is a big one.

Your future is not supposed to be wiped out because of present financial trouble.

3. Wages

Certain wages are protected, especially for lower-income individuals.

Pennsylvania also has strong protections against wage garnishment in general, which often works hand-in-hand with bankruptcy relief.

4. Public Benefits

Benefits like:

- Social Security

- Unemployment

- Workers’ compensation

are generally exempt.

These are considered essential income streams.

5. Life Insurance and Annuities

Some life insurance proceeds and annuity contracts may be exempt, depending on the structure and beneficiary.

What Pennsylvania Doesn’t Have (and Why It Matters)

Here’s where things get interesting—and why many people choose federal exemptions instead.

Pennsylvania does not provide a strong “wildcard” exemption and has limited protections for:

- Home equity

- Vehicles

- General personal property

That means if you have significant equity in a house or car, Pennsylvania exemptions alone may not fully protect you.

The Federal Exemption Comparison (Quick Snapshot)

Without going too deep into federal law, here’s why people often choose it:

- Homestead exemption (protects home equity)

- Wildcard exemption (protects anything you choose)

- More flexible coverage overall

This is why choosing the right exemption system is a strategic decision—not just a formality.

Real-World Example

Let’s say you:

- Own a home with equity

- Have a car worth $8,000

- Have some savings

Under Pennsylvania exemptions alone, you might have limited protection.

Under federal exemptions, you might be able to protect everything.

Same person. Same assets. Different outcome—just based on exemption choice.

Common Misconceptions About Exemptions

❌ “I’ll lose everything if I file.”

In reality, most Chapter 7 filers keep all or most of their property because of exemptions.

❌ “If something isn’t exempt, I automatically lose it.”

Not necessarily.

There are often ways to address non-exempt value, including:

- Buybacks

- Payment arrangements

- Chapter 13 restructuring

❌ “I don’t need to worry about exemptions.”

This is one of the biggest mistakes people make.

Exemption planning can significantly impact your outcome.

Chapter 7 vs. Chapter 13: Why Exemptions Still Matter

Chapter 7

Exemptions determine what you keep vs. what could be liquidated.

Chapter 13

Exemptions help determine how much you must repay creditors.

Even though you keep your property, exemptions still affect your payment plan.

Strategic Planning: This Is Where Attorneys Matter

Choosing exemptions isn’t just checking a box.

It requires:

- Understanding your assets

- Evaluating equity

- Comparing exemption systems

- Planning for the best outcome

A good bankruptcy attorney will walk through this with you in detail.

A Simple Way to Think About It

If bankruptcy is the reset button…

Exemptions are what you get to keep when you start over.

Final Thoughts: It’s About Protection, Not Punishment

Pennsylvania bankruptcy exemptions—and the option to use federal ones—exist for a reason:

To help you move forward, not to leave you with nothing.

So if you’re considering filing, remember:

- You likely won’t lose everything

- Exemptions protect what matters most

- Choosing the right system is critical

And most importantly:

Bankruptcy is not the end—it’s a reset with guardrails.