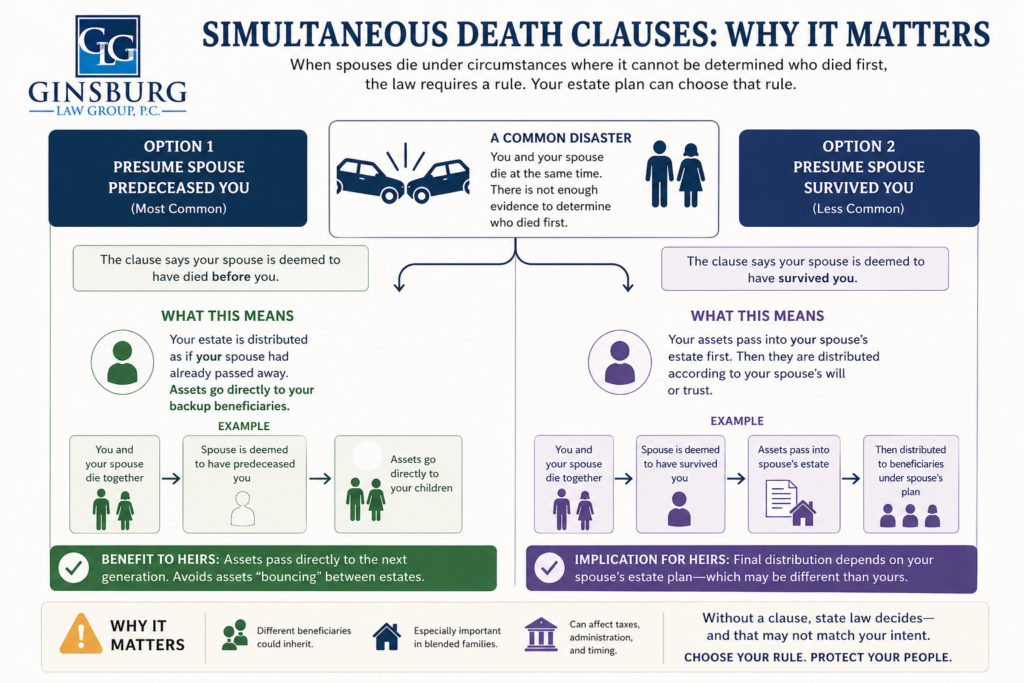

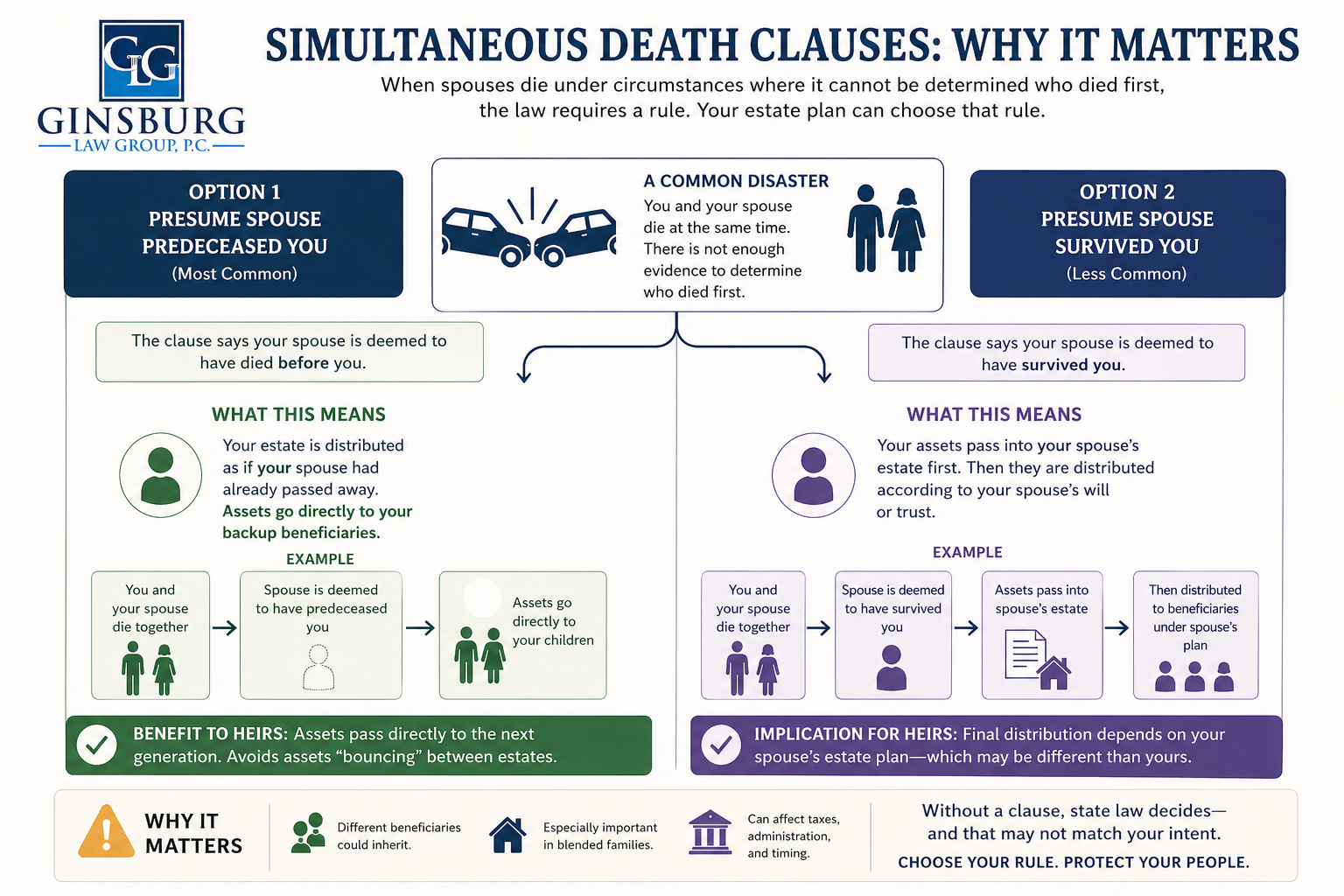

A simultaneous death clause (sometimes called a “common disaster clause”) addresses what happens when two people—typically spouses—die under circumstances where there isn’t enough evidence to determine who died first.

This can occur in situations like:

- Car accidents

- Plane crashes

- Natural disasters

- Any event where timing of death is uncertain or very close

Without clear evidence, the law has to rely on default rules—and those rules may not reflect what you would have wanted.

Why It Matters (Even Though You’re Both Gone)

At first glance, it seems irrelevant. But here’s the key:

👉 The order of death determines who inherits—and then where those assets go next.

A few seconds can change:

- Which estate receives assets first

- Whether estate taxes apply differently

- Whether assets go to your children… or someone else entirely

In short, it affects who ultimately benefits from everything you’ve worked for.

The Two Main Approaches

When drafting a will or trust, there are generally two ways to handle simultaneous death.

Option 1: Presume Your Spouse Predeceased You

This is one of the most common approaches. The clause says:

If we die simultaneously, treat my spouse as having died before me.

What This Means

- Your estate is distributed as if your spouse had already passed away

- Assets go directly to your backup beneficiaries (often children)

Example

- Husband and Wife die together

- Will says spouse is primary beneficiary, children are secondary

- Clause presumes spouse died first

👉 Result: Assets go directly to the children

Why People Choose This

- Ensures assets go straight to the next generation

- Avoids assets “bouncing” between estates

- Can simplify administration

Option 2: Presume Your Spouse Survived You

Less common, but sometimes used. This clause says:

If we die simultaneously, treat my spouse as having survived me.

What This Means

- Your assets pass into your spouse’s estate first

- Then they are distributed according to your spouse’s will

Example

- Husband’s assets go to Wife

- Wife is deemed to have survived

- Then everything is distributed under Wife’s estate plan

👉 Result: Final distribution depends on your spouse’s documents

Why This Choice Matters for Heirs

This is where things can get complicated—and where people often don’t realize the risk.

1. Different Beneficiaries

If both spouses don’t have identical estate plans:

- One spouse’s will might leave assets to children

- The other might include:

- Stepchildren

- Siblings

- Charities

👉 The “survivor presumption” could completely change who inherits.

2. Blended Families

In second marriages or blended families, this clause is critical.

- If assets pass through one spouse’s estate:

- Children from the first marriage could be unintentionally disinherited

- If assets go directly to named beneficiaries:

- It can preserve each spouse’s intended distribution

3. Taxes and Administrative Complexity

Routing assets through two estates instead of one can:

- Increase administrative burden

- Potentially impact estate tax planning

- Delay distributions to heirs

4. Timing Requirements (Bonus Consideration)

Some estate plans include a survival period (e.g., 120 hours):

- A beneficiary must survive you by a certain number of days to inherit

- If not, they are treated as having predeceased you

This works alongside simultaneous death clauses to avoid uncertainty.

What Happens If You Don’t Have a Clause?

If your documents are silent, state law steps in.

Most states—including Pennsylvania—have adopted versions of the Uniform Simultaneous Death Act, which generally prevents property from passing back and forth between estates when the order of death is unclear.

But here’s the issue:

👉 The default law may not match your intent.

That means the state—not you—decides how your estate is handled.

The Bottom Line

Even though it feels like a technicality, a simultaneous death clause answers a critical question:

👉 Who ultimately receives your assets if the worst happens?

By choosing how to handle this scenario, you:

- Protect your intended beneficiaries

- Avoid unintended consequences

- Make things clearer and easier for your family

Final Thought

Estate planning isn’t just about what happens when everything goes as expected—it’s about planning for the unexpected.

A simple clause can make the difference between:

- Your assets going exactly where you intended

- Or ending up somewhere you never would have chosen

If you’re not sure how your current documents handle this, it’s worth taking a closer look.