A letter arrives from a company called Midland Credit Management, demanding payment for a debt you may not even recognize. Your first instinct is probably to wonder if this MCM debt collection company is even real, or if it’s some kind of scam. You’re not alone. Thousands of Americans receive these notices every year, and the confusion is understandable.

Here’s the short answer: MCM is a legitimate debt collection agency, one of the largest in the country. But “legitimate” doesn’t mean you should automatically pay or ignore their attempts to contact you. Debt collectors, even lawful ones, must follow strict federal rules under the Fair Debt Collection Practices Act (FDCPA), and violations happen more often than you might think.

At Ginsburg Law Group, we represent consumers facing aggressive debt collection tactics, FDCPA violations, and credit reporting errors. This guide breaks down who MCM is, how to verify any debt they claim you owe, and the steps you can take to protect your rights and your finances.

What an MCM debt collection company is

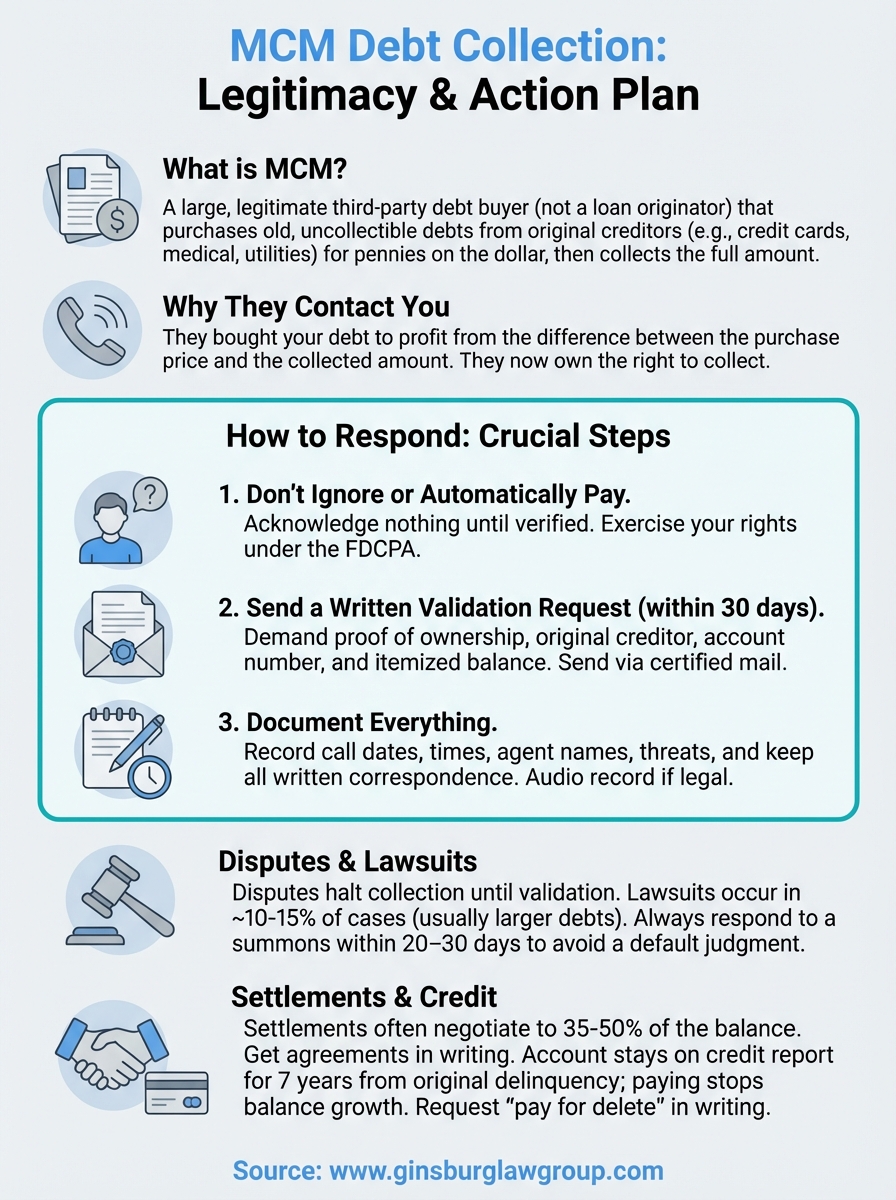

Midland Credit Management, commonly referred to as MCM, is a third-party debt collection agency headquartered in San Diego, California. The company purchases old debts from original creditors (like credit card companies, banks, and utilities) for pennies on the dollar, then attempts to collect the full amount owed from you. MCM doesn’t originate loans or credit, they simply buy the right to collect debts that creditors have written off as uncollectible.

When your original creditor decides a debt is too difficult or expensive to collect, they often sell it to companies like MCM. This sale happens without your consent, and the original creditor typically receives only a fraction of what you owed. MCM then becomes the legal owner of that debt and pursues collection through phone calls, letters, and sometimes lawsuits.

Understanding that MCM bought your debt for a fraction of its value gives you leverage when negotiating settlements.

The business model behind MCM

Debt buyers like MCM profit from volume, purchasing thousands of accounts in bulk portfolios. The original creditor may receive as little as 4 to 15 cents for every dollar of debt sold, depending on how old the account is and how likely it seems to collect. MCM then attempts to recover the full balance plus any interest or fees they’re legally allowed to add.

This business model means MCM has room to negotiate. Since they purchased your debt at a steep discount, even accepting 40% or 50% of the balance still generates profit for them. Your leverage increases if the debt is old, if you dispute its validity, or if MCM has violated collection laws during their attempts to reach you.

MCM’s parent company and scale

MCM operates as a subsidiary of Encore Capital Group, one of the largest debt buyers in North America. Encore manages billions of dollars in consumer debt across multiple collection brands. This mcm debt collection company handles millions of accounts annually, making it one of the most active players in the debt collection industry.

The scale of their operation means MCM uses automated systems, call centers, and legal teams to process collections efficiently. However, large-scale operations also lead to errors. Account information gets mixed up, statute of limitations violations occur, and FDCPA violations happen when collectors don’t follow proper procedures. Documentation from the original creditor may be incomplete or missing entirely, which weakens their legal position if you dispute the debt.

Why MCM contacts you and who they collect for

MCM contacts you because they purchased a debt that an original creditor claimed you owed and failed to pay. The original creditor sold your account after deciding it was no longer worth their time or resources to pursue collection directly. This transfer of debt ownership happens routinely in the financial industry, and MCM now holds the legal right to attempt collection on that account.

Your account typically reaches MCM after sitting unpaid for several months or years. Most creditors try their own collection efforts first, then sell accounts in bulk portfolios when those efforts fail. MCM operates as a debt buyer, not just a collection agency hired by creditors, which means they own the debt outright and keep 100% of whatever they collect.

MCM doesn’t need your permission to buy your debt, but they must prove they own it if you dispute the claim.

Types of debts MCM purchases

Credit card debt represents the largest category of accounts this mcm debt collection company handles. They also purchase medical bills, utility accounts, personal loans, and retail store credit that went unpaid. Auto deficiencies after repossession, gym memberships, and telecommunications bills (phone, internet, cable) also appear frequently in their portfolios.

Original creditors who sell to MCM

Major credit card issuers like Capital One, Citibank, and Discover regularly sell charged-off accounts to MCM. Banks sell personal loan defaults, while utilities and telecommunications companies offload unpaid service bills. Healthcare providers and hospital systems sell medical debt after internal collection attempts fail. Retail store credit programs from department stores and online retailers also end up in MCM’s portfolios.

How to respond to MCM the right way

Your first response to MCM determines your leverage throughout the entire collection process. Most consumers make critical mistakes in their initial contact, either by acknowledging debts they don’t owe or by providing information that strengthens MCM’s position. Your rights under the FDCPA require specific actions from debt collectors, and you should use these protections strategically from the very first letter or phone call.

Never discuss payment or acknowledge the debt until you’ve verified everything in writing. This mcm debt collection company must prove they own your debt and that the amount they claim is accurate. Your response sets the tone for whether MCM treats you as an informed consumer who knows their rights or as someone they can pressure into quick payment.

Requesting validation in writing protects you legally and forces MCM to prove their case before you engage further.

Request debt validation in writing

Send a debt validation letter within 30 days of receiving MCM’s initial notice. The FDCPA gives you this window to dispute the debt and demand proof. Your letter should request the original creditor’s name, the original account number, documentation showing MCM purchased the debt, and an itemized accounting of the balance including any fees or interest they added.

MCM must stop all collection activity until they provide adequate validation. Mail your request via certified mail with return receipt, which proves they received your dispute. Keep copies of everything you send and receive, as this documentation becomes crucial if violations occur or if you later negotiate a settlement.

Document every interaction

Write down the date, time, and content of every phone call from MCM. Note the collector’s name, any threats or pressure tactics, and whether they called outside permitted hours (before 8 a.m. or after 9 p.m. your local time). Record calls if your state allows one-party consent, as audio evidence strengthens FDCCA violation claims.

Save all letters, emails, and text messages in a dedicated folder. These records prove patterns of harassment, verify what MCM claimed about the debt, and document any inconsistencies in the amounts they demand.

How disputes and lawsuits with MCM work

Disputing a debt with MCM triggers specific legal protections under the FDCPA, while ignoring their attempts to collect can lead to a lawsuit that damages your finances far beyond the original debt. MCM must halt collection efforts once you send a proper validation request, but they can resume if they provide adequate proof of the debt’s validity. Understanding both the dispute process and the lawsuit timeline helps you make informed decisions about whether to fight, settle, or seek legal representation.

Most disputes with this mcm debt collection company resolve through verification requests and negotiation, but approximately 10-15% of their accounts eventually result in lawsuits. The decision to sue depends on the debt amount, your state’s statute of limitations, and whether MCM has sufficient documentation to win in court. Accounts under $1,000 rarely see lawsuits due to cost considerations, while larger balances attract more aggressive legal action.

Responding to a lawsuit is mandatory; ignoring it guarantees MCM wins a default judgment against you.

What happens when you dispute the debt

MCM must provide validation within 30 days of your written request, including proof they own the debt and documentation from the original creditor. Their response often includes a letter stating the original creditor’s name, the account number, and the balance they claim you owe. However, many validation attempts fail to meet legal standards because MCM lacks complete records from the original creditor.

If their validation appears inadequate, you can send a second dispute letter pointing out specific deficiencies. Common problems include missing signatures, incorrect account numbers, or failure to prove the chain of ownership between the original creditor and MCM.

When MCM files a lawsuit

MCM typically files lawsuits in your county’s civil court after several months of unsuccessful collection attempts. You receive a summons and complaint detailing the amount owed and giving you 20-30 days to respond, depending on your state. Failing to respond results in a default judgment, which allows MCM to garnish wages, freeze bank accounts, or place liens on property.

Responding to the lawsuit requires filing an answer that admits, denies, or claims insufficient knowledge of each allegation. Affirmative defenses include statute of limitations violations, lack of standing (MCM cannot prove they own the debt), or FDCPA violations during collection.

How settlements and credit reporting work

Settling with MCM often costs 40-60% of the claimed balance, as they purchased your debt for far less than face value and still profit from partial payment. Your credit report shows MCM’s activity from the moment they purchase your account, and their reporting practices directly affect your credit score for up to seven years. Understanding both settlement mechanics and credit reporting rules helps you negotiate better terms while minimizing long-term damage to your credit profile.

This mcm debt collection company reports to all three major credit bureaus (Equifax, Experian, and TransUnion), updating your account status monthly. Settlements appear as “settled” or “paid for less than owed”, which looks better than an unpaid collection but still hurts your score. The reporting clock starts from your original delinquency date with the first creditor, not when MCM bought the debt.

Settlement negotiations carry more weight when you request a “pay for delete” agreement in writing before sending payment.

Negotiating payment amounts

Start your settlement offer at 25-30% of the balance they claim you owe, as MCM likely paid only 10-15 cents per dollar for your debt. They will counter with a higher percentage, typically 50-70% initially, but persistent negotiation often lands between 35-50%. Your leverage increases if the debt approaches your state’s statute of limitations or if you’ve documented FDCPA violations during their collection attempts.

Never agree to payment terms verbally or provide bank account information until you receive written confirmation of the settlement amount and terms. Request that MCM delete the tradeline entirely from your credit reports as part of the settlement, though they may refuse this condition.

Understanding credit report impact

MCM’s collection account remains on your credit report for seven years from the date you first fell behind with the original creditor, regardless of when you settle. Paying or settling stops the balance from growing, but the negative mark continues reporting until the seven-year period expires. Dispute any inaccuracies in how MCM reports the account, including wrong balances, incorrect dates, or accounts you never authorized.

A quick plan going forward

Your next steps depend on whether MCM’s debt is valid and whether you have the resources to pay or settle. If you haven’t already, send a debt validation letter immediately to force this mcm debt collection company to prove ownership and accuracy. Review their response carefully for missing documentation, incorrect amounts, or procedural violations that weaken their legal position.

Document everything MCM does from this point forward, including calls outside permitted hours, threats, or misrepresentations about the debt. These violations give you leverage in settlement negotiations and potential grounds for a counterclaim under the FDCPA. If MCM files a lawsuit, respond within your state’s deadline to avoid default judgment.

Dealing with debt collectors requires knowledge of your legal rights and strategic action based on your specific situation. When collection tactics cross legal boundaries or when you need representation against aggressive debt buyers, Ginsburg Law Group helps consumers fight back against FDCPA violations and unfair debt collection practices. We offer free case evaluations to review your options and protect your financial future.