Before you fire off a single letter or make a phone call, it's critical to understand the legal ground you're standing on. When you spot an inaccurate late payment dragging down your credit score, you’re not just asking for a favor. You're exercising a powerful consumer right, one that’s backed by federal law and a cornerstone of consumer defense.

Know Your Rights When Disputing Late Payments

Think of consumer protection laws as your legal toolkit. Knowing these statutes gives you the confidence to challenge errors effectively and holds credit bureaus and lenders accountable for their actions.

The main piece of legislation you need to know is the Fair Credit Reporting Act (FCRA). This is your shield in the world of credit reporting. It gives you the power to demand accuracy from the credit bureaus and the companies—the "furnishers"—that report your account activity.

The FCRA: Your Shield Against Inaccurate Reporting

At its core, the FCRA is about one simple idea: you have a right to an accurate and fair credit report. When a late payment pops up that shouldn't be there, the law provides the exact mechanism to challenge it. An error isn't just a minor detail; it can cost you thousands in higher interest rates or even get you denied for a mortgage.

As a consumer law firm, we see countless situations where the FCRA becomes essential. Some of the most common scenarios include:

- Simple Clerical Errors: You paid on time, but someone on the lender's end keyed it in wrong. It happens more than you'd think.

- Incorrect Forbearance Reporting: You had a formal agreement to pause payments, but the lender reported you as late anyway. This is a clear violation.

- Misapplied Payments: The creditor cashed your check but couldn't figure out which account to apply it to, so they marked you delinquent.

- Outdated Information: That late payment from seven years ago should be long gone, but it's still haunting your report.

Here’s the key takeaway: when you notify a credit bureau about a mistake, they must act.

The FCRA requires credit bureaus to investigate your dispute, usually within 30 days. They do this by sending your claim to the original creditor. This is a legal mandate, not an optional courtesy.

This investigation requirement is what gives your dispute teeth. It flips the script and puts the burden of proof on them, not you. The bureau and the original creditor have to prove the negative mark is accurate. If they can't, the law says they must remove or correct it.

Understanding Furnisher Responsibilities

The FCRA doesn't just put the heat on Experian, Equifax, and TransUnion. It also sets clear rules for the "furnishers"—the banks, credit card issuers, and auto lenders that supply your data.

When a furnisher gets a dispute notice from a credit bureau, they can't just glance at it and reply, "Yep, it's verified." They are legally required to conduct a reasonable investigation. As you can learn in our complete guide on how to dispute credit report errors, their review must be legitimate.

Let's say your mortgage servicer received your payment but couldn't process it because you forgot to write the loan number on the check. They then report you as 30 days late. While the report might seem "accurate" from their narrow point of view, the reasonableness of their actions can be challenged. A proper dispute forces them to look again and justify why they didn't try to contact you or identify the payment.

The FDCPA and Debt Collectors

Things get even more interesting if a debt collector is involved. The Fair Debt Collection Practices Act (FDCPA) adds another layer of protection to your debt defense strategy.

For example, if you're actively disputing a late payment with the credit bureaus, a debt collector can't keep harassing you about it without first verifying the debt is valid. They are prohibited from making false or misleading representations, including claiming you owe a debt that is being legitimately disputed. Harassing you over a debt you've formally challenged is a direct violation of your rights under the FDCPA.

Knowing these laws exist is half the battle. You are not at the mercy of some faceless credit system. You are an active participant with legal protections designed to ensure you get a fair shake. This is the foundation that transforms a simple complaint into a formal, legally recognized dispute that demands a real response.

How to Find and Document Errors on Your Credit Reports

The key to getting an inaccurate late payment removed is solid proof. That means you need to put on your detective hat and dig into your credit reports. First things first: you need to get your hands on your complete credit files from all three major bureaus—Experian, TransUnion, and Equifax.

You have the right to get free weekly reports from AnnualCreditReport.com through the end of 2026. Make sure you use that specific site; it's the only one authorized by federal law, and plenty of lookalikes are out there. Once you have all three reports in front of you, the real hunt begins.

Going Beyond Obvious Mistakes

It's easy to spot a late payment on a credit card you've never owned. But from our experience in consumer law, the most successful disputes often come from finding the subtle, technical errors that most people miss.

Don't just give your reports a quick scan. You need to meticulously review the payment history for every single account, line by line. Your goal is to find any detail that makes the late payment reporting "inaccurate" or "incomplete" under the Fair Credit Reporting Act (FCRA).

Keep an eye out for these common, but often overlooked, errors:

- Incorrect Delinquency Status: Was a payment marked 60-days late when it was really only 30-days late? That’s a significant error and a valid reason to dispute.

- Outdated Negative Marks: A late payment from more than seven years ago has no business being on your report. The FCRA sets a strict timeline for how long negative information can legally haunt you.

- Payments Reported Late During a Forbearance: If you had an official agreement to pause payments—like a student loan deferment or a mortgage forbearance program—you should never have been reported as late during that period.

- Mixed File Errors: This is more common than you'd think. It happens when someone else's data, usually a person with a similar name or SSN, gets merged with your file. A late payment belonging to "John B. Smith" might end up on the report of "John C. Smith."

Understanding the Timing of Late Payment Reporting

Let's say you hit a rough patch and missed a credit card payment. Creditors typically don't report a payment as late until it's at least 30 days past the due date. This gives you a small but crucial window to make the payment before any damage is done to your credit.

But if it does get reported, the impact can be severe. A single 90-day late payment can torpedo a good credit score by over 100 points. If you know you paid on time but the creditor made a mistake, the FCRA gives you the power to challenge that error. For a deeper dive, Equifax.com explains how late payments are reported and impact your score.

Building Your Dispute File

Once you've zeroed in on an error, it's time to gather the evidence to prove it. Don't just rely on your memory. Create a dedicated "dispute file" for each individual error you're challenging. This organized approach is absolutely critical for showing the credit bureau exactly why their information is wrong.

A well-documented dispute file is your most powerful tool. It transforms your claim from a simple complaint into a formal, evidence-backed challenge that the credit bureaus and furnishers are legally required to take seriously under the FCRA.

Your file needs to contain copies—never send your originals!—of any document that backs up your side of the story.

This could include things like:

- Bank Statements: Highlight the transaction showing the payment cleared and the date it was processed.

- Payment Confirmations: Save any confirmation emails or screenshots you have from online payment portals.

- Correspondence with the Creditor: Keep copies of letters, emails, or even chat transcripts where you discussed a payment plan, forbearance, or billing issue.

- Your Credit Reports: Get a fresh copy of the report showing the error. Print it out and use a highlighter or pen to circle the inaccurate late payment. Make it impossible for them to miss.

For example, if a creditor reported you 60-days late but your bank statement shows a payment was made 40 days after the due date, you have concrete proof the report is inaccurate. This is the kind of hard evidence that forms the foundation of a strong dispute. If you want to dig even deeper, our guide on how to spot credit reporting errors and Metro 2 issues can help you identify more complex data-related mistakes.

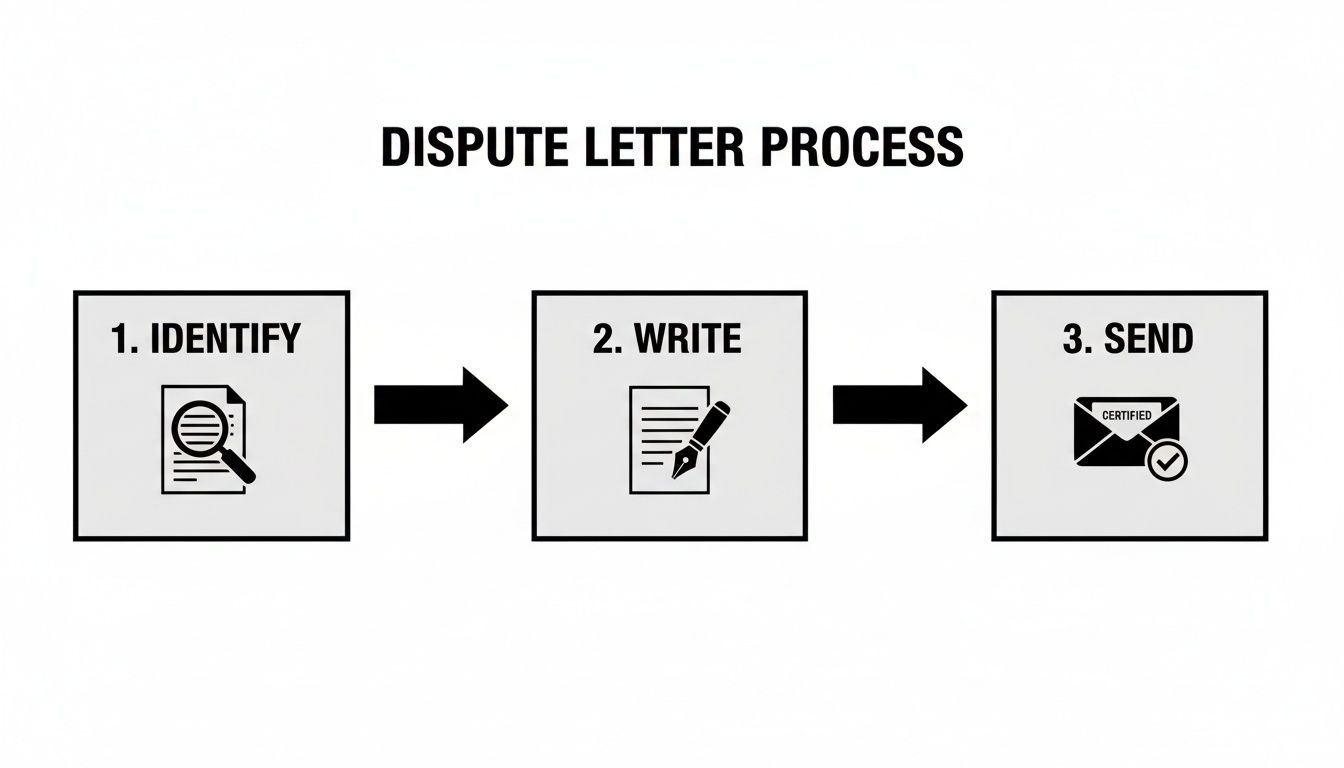

How to Write a Dispute Letter That Gets Results

So, you’ve found the error. Now it's time to take action. While the credit bureaus push you toward their online dispute forms, we always advise clients to go old-school. A formal dispute letter sent via certified mail creates a powerful paper trail that’s legally binding and much harder for them to sweep under the rug. When you're serious about protecting your consumer rights, this is your best move.

Your letter needs to be direct, factual, and sharp. This isn't the place for long, emotional stories. Your one and only goal is to present a clear, undeniable case based on the evidence you've gathered. Think of it as a formal demand for them to correct their records under your FCRA rights.

Building Your Letter: The Essential Ingredients

Treat this letter like a legal document, because that’s exactly what it is. Each piece of information is designed to trigger the credit bureau's legal obligation to investigate. We've seen too many disputes get tossed out because of a simple omission, so getting this right from the start is everything.

Your letter absolutely must include these key pieces of information:

- Your Personal Details: Start with your full name, current address, date of birth, and Social Security number. This allows the bureau to pull up your correct file without any guesswork.

- Credit Bureau Information: Make sure you're addressing the letter to the specific bureau reporting the error—Equifax, Experian, or TransUnion. You have to send a separate, tailored letter to each one.

- A Crystal-Clear Opening: Get straight to the point. A simple, direct sentence works best, like: "I am writing under my rights guaranteed by the Fair Credit Reporting Act (FCRA) to dispute an inaccurate late payment on my credit report."

- Pinpointing the Error: This is crucial. Name the creditor (the "furnisher"), the complete account number, and the exact late payment you're disputing, including the date. For instance: "The 60-day late payment reported for my Freedom Mortgage account (Loan #123456789) for May 2020 is incorrect."

By being this specific, you prevent the bureau from claiming they couldn't find the item you're talking about.

Telling Your Side of the Story (The Right Way)

This is the heart of your letter. After you’ve identified the mistake, you need to explain why it's a mistake in a few concise, fact-based sentences. You're not writing a novel, just stating the facts of your case.

For example, if you had a payment reported as late while you were in a forbearance program, you could write: "This payment was reported late during an official forbearance period that was agreed upon with the lender, which violates our agreement. I've attached a copy of the forbearance confirmation letter."

Or maybe it was a simple processing error. A recent court case involving Freedom Mortgage showed that a servicer could technically report a payment as late if they couldn't identify it. If that happened to you, but you did everything right, your dispute could state: "I mailed my payment on April 28, 2020, well before the due date. The check clearly included my loan number as instructed, and my bank statement confirms the servicer cashed it. This late payment is factually inaccurate."

To make sure your letter has everything it needs, use the following table as a final checklist. It breaks down the essential components and provides quick examples to guide you.

Key Elements of an Effective Dispute Letter

| Component | Description | Example |

|---|---|---|

| Clear Identification | Your full name, address, SSN, and date of birth. | "Jane Q. Public, 456 Oak Ave, Sometown, USA 54321" |

| Bureau's Address | The correct mailing address for the bureau's dispute department. | "Experian, P.O. Box 4500, Allen, TX 75013" |

| Account & Error Details | The creditor's name, account number, and the specific inaccurate entry. | "Citibank, Acct# … ending in 5678, 30-day late payment reported for July 2025." |

| Reason for Dispute | A brief, factual statement explaining why the entry is incorrect. | "This account was never late. My bank statement shows a timely payment was made on the 15th." |

| Formal Request | A clear demand for the item to be removed or corrected. | "Please remove this inaccurate late payment from my credit file immediately." |

| Evidence List | A list of the documents you have enclosed as proof of your claim. | "Enclosed are copies of my bank statement and the canceled check." |

Having a complete, well-structured letter is your best tool for a successful dispute. Double-check every component before you send it.

Send It Off and Start the Clock

How you mail this letter is just as important as what you write in it. Always, always send your dispute letter via certified mail with a return receipt requested.

This isn't just a suggestion; it's a critical step that gives you legal proof of the exact date the credit bureau received your dispute. That date officially starts their 30-day investigation clock under the FCRA. Without that little green receipt card, it’s just your word against theirs.

One last thing—be sure to enclose copies of your supporting documents, never your originals. Your evidence package, with neatly organized bank statements, confirmation emails, and a highlighted copy of the credit report, should be attached right behind your letter. When you build a case this solid and send it the right way, you give yourself the best possible chance of getting that damaging late payment wiped off your report for good.

Managing the Investigation Process and Your Follow-Up

So, you’ve mailed your certified letter. Congratulations—you've officially started the clock on the credit bureau's legal duties under the Fair Credit Reporting Act (FCRA). This next phase is mostly a waiting game, but it's one with very strict rules. Knowing what happens behind the scenes is crucial to making sure your dispute gets the serious attention it deserves.

The moment a credit bureau receives your dispute, their 30-day investigation window kicks in. They can’t just ignore your letter. By law, they must forward your dispute and all the evidence you sent to the company that originally reported the information—the "furnisher."

This is where things get interesting. The furnisher, whether it’s your credit card company or mortgage lender, is then required to conduct its own reasonable investigation. They can't just robotically confirm the late payment; they have to actually review their records against the specific evidence and arguments you provided.

Tracking the Timeline and Interpreting the Results

Your main job now is to keep an eye on the calendar. That certified mail receipt is your golden ticket—it's your proof of exactly when the 30-day countdown began. Within this timeframe (which can be extended to 45 days if you send additional information), you must receive a written response from the credit bureau outlining their findings.

You're waiting for one of three things to happen:

- The item is deleted or corrected. This is the best-case scenario. The bureau confirms the late payment was inaccurate and has been removed. Your credit report gets updated, and you'll likely see a welcome bump in your score.

- The item is verified. This is the most common and frustrating outcome. The bureau says the furnisher checked its records and insists the information is accurate, so the late payment will stay put.

- You hear nothing at all. If the 30-day window slams shut and you've gotten no response, the bureau has violated the FCRA. A non-response means the disputed item must be deleted from your report.

Let’s be real: consumer frustration with this process is at an all-time high, and the data backs it up. The FTC Sentinel Network documented a shocking 95% increase in credit reporting complaints. Disputes over 'incorrect information' like the ones we're discussing led the pack with 1.4 million complaints in the second half of 2025 alone. This is fueling a 30.7% surge in FCRA lawsuits, driven by consumers fed up with bureaus and furnishers failing to perform proper investigations. You can see the full breakdown of these soaring litigation and complaint trends on bridgeforcedatasolutions.com.

What to Do If Your Dispute Is Rejected or Ignored

Getting a verification notice feels like hitting a brick wall, but it’s not the end of the road. If you're certain the late payment is an error, you still have some powerful moves to make. This is where persistence often separates success from failure in consumer rights battles.

Your first step is to consider re-disputing, especially if you have new or more compelling evidence. Sometimes a single different document can be what tips the scales in your favor. If that fails, you have the right to add a 100-word consumer statement to your credit file.

A consumer statement is your chance to add a short explanation to your credit report. While it won't remove the negative mark, it tells any future lender who pulls your credit that you formally disagree with how that item was reported.

This simple but effective process is the bedrock of a successful dispute. You identify the error, write a clear and factual letter, and send it via certified mail.

Following this systematic, evidence-based approach gives you the best possible chance of correcting inaccuracies on your credit report.

Dealing With Debt Collectors During a Dispute

It's a common—and illegal—tactic. While you’re in the middle of disputing a late payment with the bureaus, a debt collector starts calling you about that same account. This is where your rights under the Fair Debt Collection Practices Act (FDCPA) become your shield.

If a collector contacts you about an account you're actively disputing, immediately inform them in writing that the debt is under dispute. The FDCPA requires them to stop all collection efforts until they have verified the debt. Any attempt to keep pressuring you for payment on a disputed item is a clear violation of federal law and can be grounds for legal action. As a consumer law firm, we at Ginsburg Law Group PC see this all the time and help clients hold these collectors accountable.

When the System Fails: Escalating Your Dispute and Getting Legal Help

So, you’ve done everything by the book. You sent a detailed dispute letter with rock-solid proof by certified mail, but the credit bureau or your creditor is still stonewalling you. When a clear mistake remains on your report after all that, you've hit the limit of what you can do on your own. It's time to escalate.

Your first move should be to file a complaint with the Consumer Financial Protection Bureau (CFPB). Think of the CFPB as a powerful government watchdog. Filing is free, and it puts your complaint into a formal system that companies are required to respond to. Often, just getting the CFPB involved is enough to make a previously unresponsive company finally pay attention.

But what if even the CFPB can’t get the job done? That’s your signal that you’ve reached the point where you need a legal professional in your corner.

Knowing When to Call a Consumer Law Attorney

Sometimes, another letter just isn’t going to cut it. Bringing in a consumer law firm like Ginsburg Law Group becomes your most powerful option when it’s clear your rights are being ignored.

You likely have a strong case for legal action if you're running into these all-too-common brick walls:

- The Creditor "Verifies" Without Investigating: You send undeniable proof of the error, but the creditor simply "verifies" the debt is accurate without doing any real digging. This is a classic violation of their duties under the Fair Credit Reporting Act (FCRA).

- The Credit Bureau Misses the Deadline: The bureau blows right past its 30-day investigation window and never sends you the results. By law, they are supposed to delete the disputed item if they can't investigate it in time.

- Your Dispute Is Ignored as "Frivolous": The bureau dismisses your valid, well-documented dispute as "frivolous" without giving you a legitimate reason why.

- The Error Comes Back from the Dead: The inaccurate late payment gets removed, only to mysteriously reappear on your report a few months later. This is often an illegal re-reporting of information you already disputed.

If an inaccurate late payment has caused you tangible financial harm—like getting denied for a mortgage, being forced into a high-interest car loan, or even losing a job offer—you may have a strong case for damages. This is exactly when professional legal help becomes non-negotiable.

How the FCRA Makes Legal Help Affordable

Many people get nervous about hiring an attorney, immediately thinking about the cost. But the FCRA was specifically designed to level the playing field for consumers. It has a powerful "fee-shifting" provision built right into the law.

What does that mean for you? It means that if you sue a credit bureau or creditor for violating your rights and you win, the court can order them to pay your attorney's fees and legal costs. This provision makes it possible for anyone to fight back, regardless of what's in their bank account.

The financial sting of a single error is no small thing. One 90+ day late payment can crater a FICO score by as much as 133 points. According to recent consumer credit statistics on ConsumerAffairs.com, that kind of drop can easily knock your credit from 'Very Good' to 'Fair,' costing you thousands over the life of a loan. It's no wonder credit reporting issues have become the top complaint category at the FTC.

Your Next Step When You're Out of Options

When you're dealing with a stubborn creditor or a non-compliant credit bureau, you need an advocate who lives and breathes this area of law. At Ginsburg Law Group PC, our work is focused on defending consumers and pursuing FCRA lawsuits. We’ve seen all the tricks and tactics companies use, and we know how to hold them accountable.

If you believe your rights have been violated, start documenting everything. A detailed paper trail is the single most important asset in a potential lawsuit. To make sure you're saving the right things, check out our guide on how to preserve evidence for a credit reporting lawsuit. You don’t have to just accept a flawed credit report that’s holding you back.

Frequently Asked Questions About Disputing Late Payments

Even with a solid plan, you're bound to run into questions when you start digging into your credit reports. Specific situations come up that can be confusing. Let's tackle some of the most common questions people ask when they set out to challenge a late payment.

Can I Dispute a Late Payment That Was Actually My Fault?

Technically, no—at least not with a formal FCRA dispute. The Fair Credit Reporting Act is all about correcting inaccurate information. If you genuinely paid late and the creditor reported it correctly, a dispute with the bureaus will almost certainly be verified and closed.

But you're not out of options. Your best bet is to write a "goodwill adjustment" letter directly to your original creditor. This isn't a demand; it's a polite request asking them to remove the negative mark as a courtesy.

This strategy has the highest chance of success if you have an otherwise stellar payment history with that company. Explain what happened, emphasize your loyalty as a customer, and ask for a one-time pass. It's never guaranteed, but we've seen it work for many consumers. It’s always worth a shot.

How Long Does a Late Payment Stay on My Credit Report?

A legitimate late payment can stick to your credit report for up to seven years. That timeline is set by the FCRA and it’s a hard rule.

The silver lining is that its impact fades over time. A five-year-old late payment is a minor annoyance compared to one from just a few months ago. Still, if you want it gone before that seven-year clock runs out, your only path is to find an inaccuracy and get it removed through a successful dispute.

Should I Dispute With the Credit Bureau or the Creditor?

Both have their place, but you should always start with the credit bureaus. When you file a formal dispute with Experian, TransUnion, or Equifax, you trigger their legal obligation under the FCRA to investigate your claim.

This official process forces the bureau to contact the creditor (the "furnisher") and demand they verify the debt. While going straight to the creditor can sometimes resolve simple errors faster, the formal bureau dispute creates the critical paper trail you'll need if things get complicated and you have to escalate the issue later.

Worried about repercussions? Don't be. Filing a dispute has absolutely no negative impact on your credit score. It's a protected consumer right. If you win, your score will almost certainly go up. If you lose, it just stays the same.

Will Disputing a Late Payment Hurt My Credit Score?

Absolutely not. The act of filing a dispute has zero effect on your credit score. Think of it as a neutral action.

If your dispute is successful and the late payment gets deleted, your score will likely get a nice boost. If the creditor verifies the information and the dispute is denied, your score simply remains where it was. You have nothing to lose by exercising your rights to ensure your report is accurate.

If you've followed all the steps and are still hitting a wall with creditors or the bureaus, you don't have to give up. When your rights under the FCRA or FDCPA are being ignored, it may be time to get legal help. At Ginsburg Law Group PC, we specialize in fighting for consumers against unfair credit reporting and illegal debt collection practices. If you need an advocate on your side, contact us to see how we can help.