Summary

Debt collection lawsuits are surging nationwide, and the reason is simple: many collectors are still violating the FDCPA. From failing to validate debts to misrepresenting balances and illegally repossessing vehicles, consumers are fighting back — and winning. If you’ve been contacted by a collector, don’t assume they’re following the law. You may have rights even if you owe the debt.

1/12/26-Across the country, debt collectors are being sued at record levels — and for many of the same mistakes they’ve been making for years.

Recent federal court filings show a sharp increase in lawsuits brought under the Fair Debt Collection Practices Act (FDCPA). These cases aren’t about technical loopholes. They’re about real consumers being misled, harassed, or pressured into paying debts in ways the law simply does not allow.

Here’s what we’re seeing — and what it means for you.

What We’re Seeing Nationally

Federal courts are flooded with new FDCPA cases in 2026. The volume alone tells an important story:

debt collectors are still failing to follow the law, even though the rules are well-established.

The cases span nearly every state and involve:

- Large national debt buyers

- Collection law firms

- Medical debt collectors

- Auto lenders and repossession agents

- Mortgage servicers and collection vendors

Many of these lawsuits allege violations that occur before a consumer ever sets foot in court — during letters, phone calls, credit reporting, or repossession attempts.

The Most Common FDCPA Violations We’re Seeing

While every case is different, the same violations appear again and again:

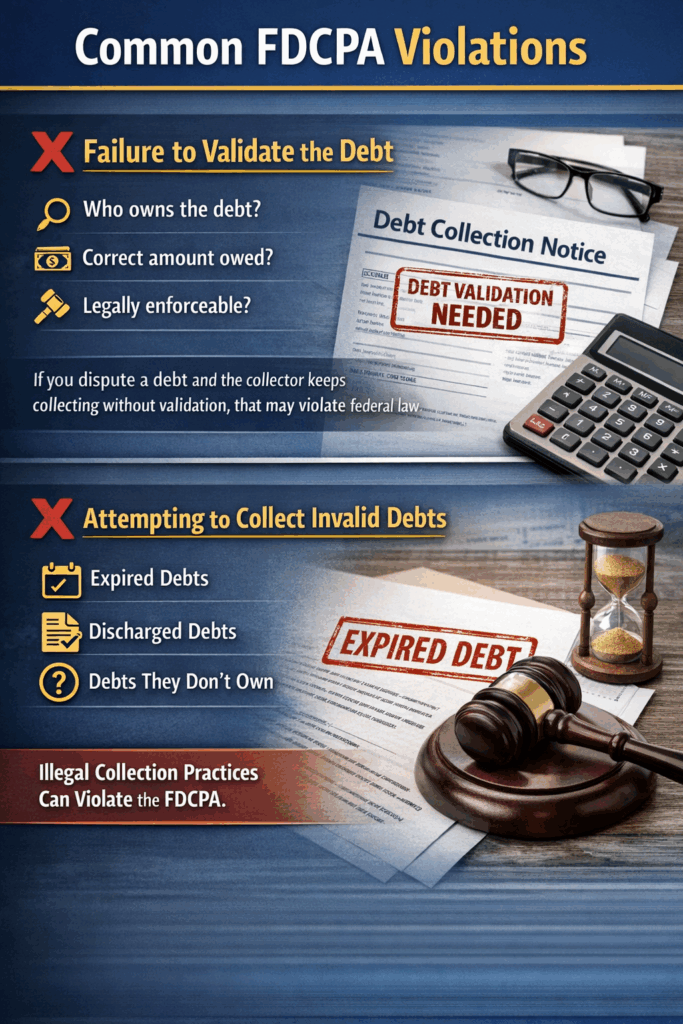

❌ Failure to Validate the Debt

Collectors continue to demand payment without properly verifying:

- Who owns the debt

- The correct amount owed

- Whether the debt is legally enforceable

If you dispute a debt and the collector keeps collecting without validation, that may violate federal law.

❌ Trying to Collect Time-Barred or Void Debts

We are seeing numerous cases where collectors attempt to collect:

- Debts past the statute of limitations

- Debts previously discharged or resolved

- Debts they do not legally own

Attempting to collect a debt that is not legally enforceable can violate the FDCPA.

❌ Misrepresenting the Amount or Legal Status of a Debt

This includes:

- Inflated balances

- Incorrect interest or fees

- Claiming a lawsuit is imminent when it isn’t

- Suggesting wages will be garnished without a judgment

Even small inaccuracies can be actionable.

❌ Illegal Repossession Conduct

Repossession agents are not exempt from the FDCPA. We continue to see lawsuits involving:

- Threatened or completed repossessions without legal authority

- Repossessions involving deception or intimidation

- Taking vehicles without the right to do so

Federal law strictly limits what repossession agents can do.

❌ Credit Reporting Without Proper Dispute Notices

Collectors must report disputed debts accurately.

Failing to mark a debt as “disputed” after notice is a frequent violation.

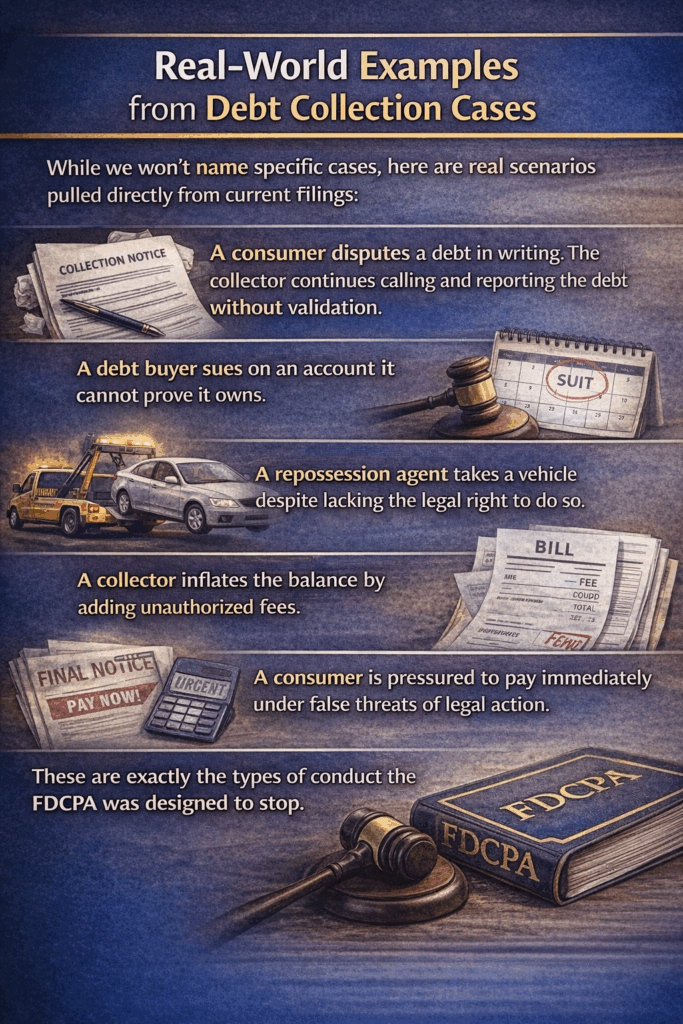

Real-World Examples

While we won’t name specific cases, here are real scenarios pulled directly from current filings:

- A consumer disputes a debt in writing. The collector continues calling and reporting the debt without validation.

- A debt buyer sues on an account it cannot prove it owns.

- A repossession agent takes a vehicle despite lacking the legal right to do so.

- A collector inflates the balance by adding unauthorized fees.

- A consumer is pressured to pay immediately under false threats of legal action.

These are exactly the types of conduct the FDCPA was designed to stop.

What Consumers Should Do If Contacted by a Debt Collector

Before paying anything, take these steps:

- Do not assume the debt is valid

- Do not give bank or payment information

- Request written validation of the debt

- Save all letters, emails, and voicemails

- Do not ignore court papers — but do not respond without advice

Even if you owe money, you still have rights.

Call Us Before You Pay or Respond

Many FDCPA cases cost consumers nothing out of pocket.

The law allows for:

- Statutory damages up to $1,000

- Actual damages

- Attorney’s fees paid by the debt collector

If you’ve been contacted by a debt collector, threatened with repossession, or sued on a questionable debt, call us first at 855-978-6564.

Paying too quickly can mean giving up valuable rights.

")