(“Wait… Tennessee has its own exemptions AND I can choose federal?”)

Yes—and that choice can make a big difference in your case.

If you’re filing bankruptcy in Tennessee, understanding exemptions isn’t just helpful—it’s essential. The exemption system you choose will directly impact what property you keep, what’s protected, and how your case plays out.

The good news? Tennessee gives you options.

Let’s break it all down in a way that actually makes sense.

First: What Are Bankruptcy Exemptions?

At the most basic level:

Exemptions are laws that protect your property when you file bankruptcy.

Without exemptions, the bankruptcy process could allow creditors to take everything you own.

With exemptions, the law ensures you can keep:

- Basic necessities

- Essential property

- The foundation for a fresh start

Think of exemptions as a legal shield between you and losing everything.

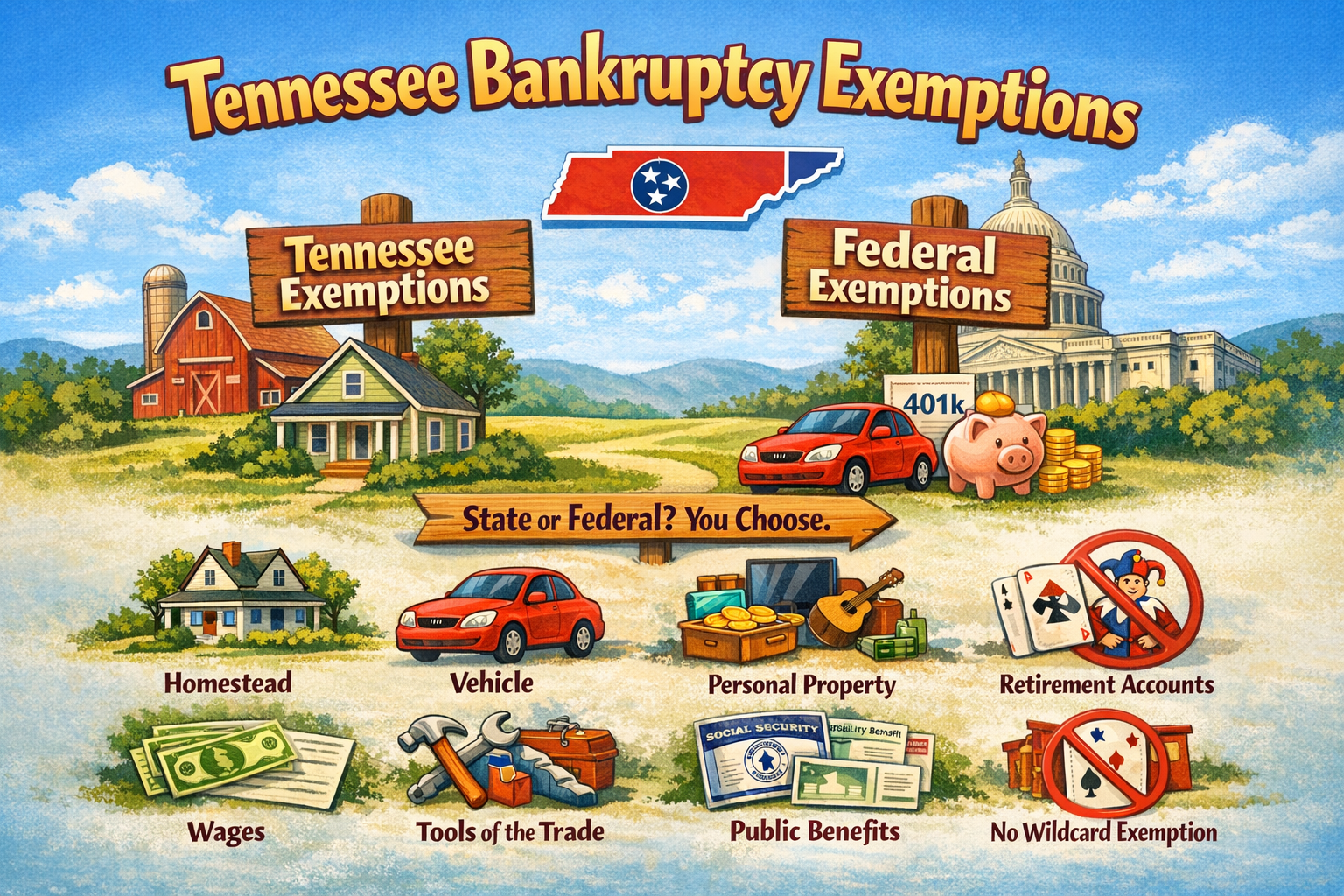

Tennessee Gives You a Choice: State vs. Federal Exemptions

Here’s where Tennessee stands out:

You can choose between Tennessee exemptions OR federal bankruptcy exemptions.

But you cannot mix and match—you must pick one system.

Why this matters:

Each system has strengths and weaknesses. Choosing the right one depends on:

- Whether you own a home

- How much equity you have

- The value of your car

- Whether you have cash or savings

- Your overall asset picture

This is not a one-size-fits-all decision.

How Exemptions Work (Simple Example)

Let’s say:

- Your car is worth $8,000

- You owe $3,000 on it

- Your equity is $5,000

If your exemption protects up to $10,000 in vehicle equity, your car is fully protected.

If it only protects $3,000, then $2,000 may be considered non-exempt.

But even then, that doesn’t automatically mean you lose the car—it just means strategy comes into play.

Tennessee Exemptions: The Key Categories

Let’s look at what Tennessee law actually protects.

1. Homestead Exemption (Your Home)

This is one of the most important protections.

Tennessee Homestead Limits (approximate ranges):

- $5,000 – single filer

- $7,500 – joint owners

- $12,500 – age 62+

- Up to $25,000 – certain older married filers

What it protects:

Equity in your primary residence.

The reality:

Tennessee’s homestead exemption is relatively low compared to federal exemptions.

This is why many homeowners in Tennessee choose the federal system instead.

2. Personal Property Exemption

Tennessee provides a general personal property exemption.

Typical amount:

- Around $10,000 total (varies depending on filing status)

Covers:

- Furniture

- Electronics

- Clothing

- Bank accounts

- Miscellaneous personal items

This is a flexible exemption—but it has limits.

3. Motor Vehicle Exemption

Typical protection:

- Around $10,000 in vehicle equity

This is relatively strong compared to some states.

Example:

- Car value: $12,000

- Loan: $4,000

- Equity: $8,000

Fully protected.

4. Retirement Accounts

Good news:

Most retirement accounts are fully protected.

This includes:

- 401(k)s

- IRAs

- Pensions

This is one of the strongest and most consistent protections across bankruptcy law.

5. Wages

Tennessee protects a portion of your wages, especially:

- Disposable earnings

- Income necessary for support

Tennessee also has wage garnishment limits that interact with bankruptcy protections.

6. Public Benefits

These are generally fully exempt:

- Social Security

- Disability benefits

- Unemployment

- Veterans benefits

These are considered essential and protected.

7. Tools of the Trade

If you rely on tools for your job (contractor, mechanic, etc.), Tennessee allows exemptions for those tools up to a certain value.

8. Life Insurance

Some life insurance policies and proceeds may be exempt, depending on structure and beneficiary.

What Tennessee Does NOT Have (And Why It Matters)

Here’s a big limitation:

Tennessee does NOT have a strong wildcard exemption.

That means:

- Less flexibility

- Harder to protect cash or miscellaneous assets

- More planning required

This is a major reason why many filers consider federal exemptions instead.

Federal vs. Tennessee Exemptions: How to Choose

When Tennessee exemptions might work well:

- You have modest assets

- You don’t own a home (or have little equity)

- Your property fits neatly into Tennessee categories

When federal exemptions may be better:

- You have home equity

- You need a wildcard to protect cash or savings

- You want more flexibility

Real-World Comparison

Let’s say you have:

- $15,000 home equity

- $5,000 in savings

- $6,000 car equity

Under Tennessee exemptions:

- Home may not be fully protected

- Savings may be partially exposed

- Car likely protected

Under federal exemptions:

- Home may be fully protected

- Savings protected using wildcard

- Car protected

Same situation—very different outcomes.

Chapter 7 vs. Chapter 13 in Tennessee

Chapter 7

- Exemptions determine what you keep

- Non-exempt assets could be liquidated

Chapter 13

- You keep everything

- You repay creditors based on non-exempt value

Exemptions still matter because they affect your payment plan.

Common Mistakes People Make

❌ “I’ll lose everything if I file.”

Reality:

Most people keep most—or all—of their property.

❌ “I should choose Tennessee exemptions because I live here.”

Not necessarily.

Federal exemptions are often better.

❌ “Cash is safe.”

Cash is one of the least protected assets without proper planning.

❌ “I don’t need to think about exemptions.”

This is a major mistake.

Exemption strategy can completely change your case outcome.

Strategic Planning Matters

Before filing, people sometimes:

- Time their filing carefully

- Pay necessary expenses

- Allocate assets strategically

Important:

This must always be done legally and transparently.

Never hide assets. Always disclose everything.

The Emotional Reality

Let’s be honest:

The biggest fear people have is losing everything.

Understanding Tennessee exemptions changes that.

Instead of panic, you get clarity.

Instead of fear, you get a plan.

A Simple Way to Think About It

If bankruptcy is the reset button…

Exemptions determine what you keep when you restart.

Why Tennessee Filers Need Good Advice

Because Tennessee’s system is:

- More limited than some states

- Less flexible without a wildcard

- Highly dependent on strategy

Choosing between state and federal exemptions is not something you want to guess on.

Practical Tips

1. List Everything

- Bank accounts

- Vehicles

- Property

- Digital assets

2. Don’t Forget Cash

Cash is often overlooked—and vulnerable.

3. Compare Both Systems

Never assume one is better.

4. Work With an Experienced Attorney

This is where experience matters most.

Final Thoughts: Protection Is the Goal

Tennessee bankruptcy exemptions—whether state or federal—exist to:

- Protect what you need

- Help you rebuild

- Give you a fresh start

So if you’re considering filing, remember:

- You have options

- You likely won’t lose everything

- Strategy makes a huge difference

And most importantly:

Bankruptcy is not about starting over with nothing—it’s about starting over with what you need to move forward.