(“So… what am I allowed to keep if I file bankruptcy in Maryland?”)

That’s the question everyone asks—and the answer is usually much better than people expect.

If you’re filing bankruptcy in Maryland, understanding exemptions is the key to reducing fear and gaining control. These laws determine what property you get to keep, what’s protected, and how your case will unfold.

And unlike some states, Maryland has its own unique system—with a few quirks that make strategy especially important.

Let’s break it all down.

First: What Are Bankruptcy Exemptions?

At their core:

Exemptions are laws that protect your property when you file bankruptcy.

Without exemptions, creditors could potentially take everything you own.

With exemptions, the law allows you to keep:

- Essential assets

- Basic living necessities

- The foundation for a financial reset

Think of exemptions as a legal shield around your most important property.

Maryland Is an “Opt-Out” State

Here’s a critical rule:

Maryland requires you to use Maryland exemptions—you cannot use federal exemptions.

This is different from states like Tennessee or Pennsylvania, where you can choose between state and federal systems.

In Maryland, you’re working with one set of rules—so understanding them is essential.

How Exemptions Work (Simple Example)

Let’s say:

- You own a car worth $7,000

- You owe $4,000

- Your equity is $3,000

If Maryland allows you to protect that amount of vehicle equity, your car is safe.

If your equity exceeds the exemption, the extra portion may need to be addressed—but that doesn’t automatically mean you lose the asset.

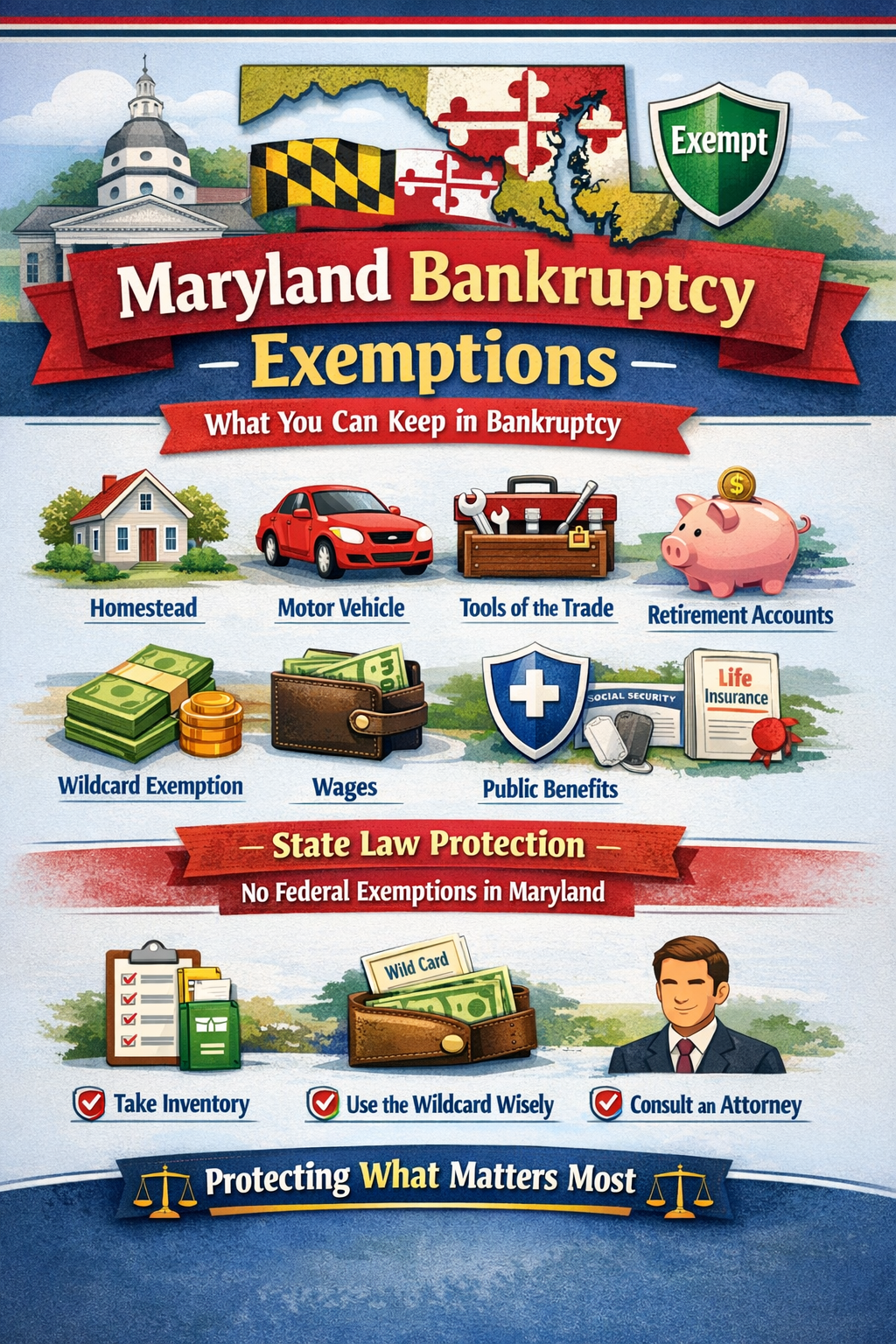

Maryland Exemptions: The Key Categories

Let’s walk through the most important protections available under Maryland law.

1. Homestead Exemption (Your Home)

Protection:

- Around $25,000 per individual

- Up to $50,000 for married couples filing jointly

What it covers:

Equity in your primary residence.

Example:

- Home value: $300,000

- Mortgage: $260,000

- Equity: $40,000

If you’re filing jointly, you may be able to fully protect that equity.

Important Note:

Maryland’s homestead exemption is modest compared to some states (like Florida), but still very useful.

2. Personal Property Exemption

Maryland allows you to protect certain personal items, including:

- Clothing

- Household furnishings

- Appliances

These items typically have low resale value, so they’re often fully protected.

3. Tools of the Trade

Protection:

- Up to about $5,000 in tools, instruments, or books

Who this helps:

- Contractors

- Mechanics

- Skilled workers

If your livelihood depends on tools, this exemption matters.

4. Motor Vehicle Exemption

Protection:

- Around $5,000 in vehicle equity

Example:

- Car value: $10,000

- Loan: $6,000

- Equity: $4,000

Fully protected.

5. Retirement Accounts (Strong Protection)

Good news:

Most retirement accounts are fully protected in Maryland.

This includes:

- 401(k)s

- IRAs

- Pensions

Your long-term financial future is not meant to be wiped out by bankruptcy.

6. Wages

Maryland protects a portion of your wages, particularly:

- Disposable income

- Income necessary for basic support

Maryland also has garnishment limits that tie into these protections.

7. Public Benefits

Fully protected:

- Social Security

- Disability benefits

- Unemployment

- Veterans benefits

These are considered essential and off-limits to creditors.

8. Life Insurance and Annuities

Certain life insurance proceeds and policies may be exempt, depending on the beneficiary and structure.

The “Wildcard” Exemption (Maryland’s Version)

Here’s where Maryland gets interesting.

Maryland provides a wildcard-style exemption that allows you to protect:

👉 Up to $6,000 in any property

This can be applied to:

- Cash

- Bank accounts

- Additional vehicle equity

- Personal property

Why this matters:

This is one of the most flexible tools you have.

If something doesn’t fit neatly into another category, the wildcard can protect it.

What Happens If an Asset Exceeds the Exemption?

This is where people get nervous—but let’s simplify it.

If an asset exceeds exemption limits:

In Chapter 7:

- The trustee may look at the non-exempt portion

- But you may have options (like paying that value to keep the asset)

In Chapter 13:

- You keep the asset

- You repay creditors the non-exempt value over time

Chapter 7 vs. Chapter 13 in Maryland

Chapter 7

- Exemptions determine what you keep

- Non-exempt assets may be liquidated

Chapter 13

- You keep everything

- Exemptions determine how much you must repay

Real-World Example

Let’s say you have:

- $20,000 home equity

- $4,000 car equity

- $3,000 in savings

- Household goods

Using Maryland exemptions:

- Home = protected

- Car = protected

- Savings = protected using wildcard

- Household goods = protected

Result?

You likely keep everything.

Common Misconceptions About Maryland Exemptions

❌ “I’ll lose everything.”

Reality:

Most people keep most—or all—of their property.

❌ “Maryland exemptions are weak.”

Not necessarily.

While not as generous as some states, they are very workable with proper planning.

❌ “Cash is safe.”

Cash is often one of the most vulnerable assets—unless you use the wildcard exemption strategically.

❌ “I don’t need to think about exemptions.”

This is a big mistake.

Exemption strategy can completely change your outcome.

Strategic Planning Matters

Because Maryland is an opt-out state, you don’t have the flexibility of choosing federal exemptions.

That makes planning even more important.

Before filing, people sometimes:

- Time their filing

- Pay necessary expenses

- Allocate exemptions strategically

Important:

This must always be done legally and transparently.

Never hide assets.

The Emotional Reality

Let’s be honest:

The biggest fear people have when considering bankruptcy is:

“Am I going to lose everything?”

Understanding Maryland exemptions changes that.

Instead of fear, you get clarity.

Instead of uncertainty, you get a plan.

A Simple Way to Think About It

If bankruptcy is the reset button…

Maryland exemptions determine what you get to keep when you restart.

Why Maryland Filers Can Still Have Strong Outcomes

Even without federal exemptions, Maryland provides:

- A usable homestead exemption

- A flexible wildcard

- Strong retirement protections

- Protection for essential assets

With the right strategy, many filers keep everything they need.

Practical Tips for Maryland Filers

1. Take Inventory of Everything

List:

- Bank accounts

- Vehicles

- Property

- Digital assets

2. Don’t Forget Cash

Cash is often overlooked—and exposed.

3. Use the Wildcard Wisely

This is your most flexible protection tool.

4. Be Honest

Full disclosure is required.

5. Work With an Experienced Attorney

Maryland exemption strategy is not something you want to guess on.

Final Thoughts: It’s About Protection, Not Punishment

Maryland bankruptcy exemptions are designed to:

- Protect what you need

- Help you rebuild

- Give you a fresh start

So if you’re considering filing, remember:

- You won’t lose everything

- Exemptions protect what matters

- Strategy makes a big difference

And most importantly:

Bankruptcy isn’t about starting over from nothing—it’s about starting over with what you need to move forward.