(“I heard Florida lets you keep your house no matter what—is that true?”)

Sometimes… yes.

Florida is one of the most debtor-friendly states in the country when it comes to bankruptcy exemptions. But like most things in the law, the truth is a little more nuanced.

If you’re filing bankruptcy in Florida—or just researching your options—understanding how Florida bankruptcy exemptions work can completely change your expectations (and your outcome).

Let’s break it down in a way that actually makes sense.

First: What Are Bankruptcy Exemptions?

At the most basic level:

Exemptions are laws that protect your property when you file bankruptcy.

Without exemptions, the bankruptcy system could allow creditors to take everything you own.

With exemptions, you get to keep:

- Essential property

- Necessary income

- The foundation for a financial reset

Think of exemptions as a legal shield that protects your life while you wipe out debt.

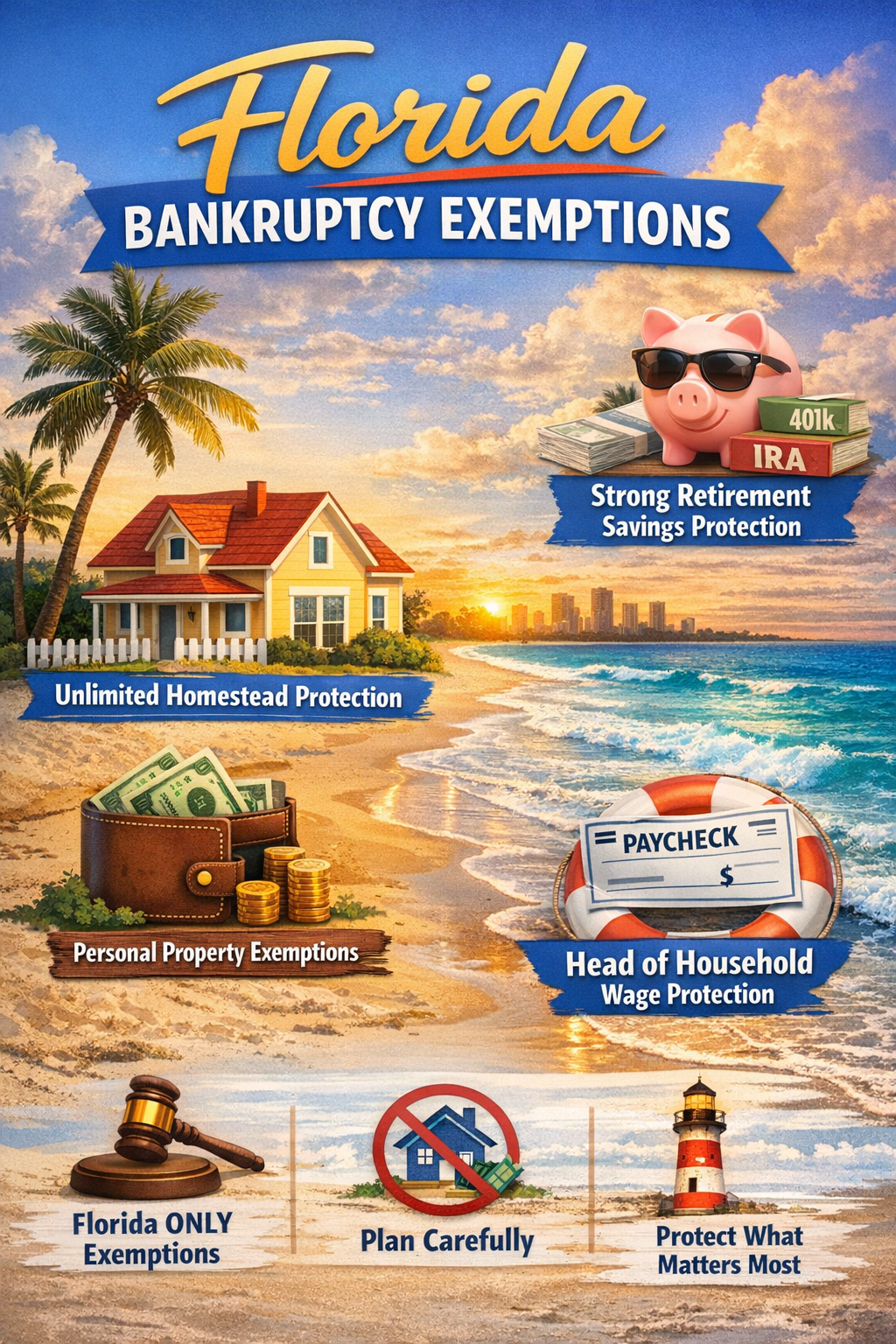

Florida Is an “Opt-Out” State (Important!)

Here’s a key rule:

Florida requires you to use Florida exemptions—you cannot use federal exemptions.

Unlike states like Tennessee or Pennsylvania, you don’t get to choose.

This matters because:

- Florida exemptions are extremely strong in some areas

- But more limited in others

The Crown Jewel: Florida’s Homestead Exemption

This is what Florida is famous for.

What it does:

Protects your primary residence.

What makes it unique:

It offers UNLIMITED protection for home equity.

Yes—unlimited.

But there are conditions:

- The property must be your primary residence

- Size limits apply:

- Up to ½ acre in a municipality

- Up to 160 acres outside a municipality

- You must meet residency requirements (generally 1,215 days for full protection)

Real-World Example:

- Home value: $600,000

- Mortgage: $200,000

- Equity: $400,000

In many states, that level of equity would be at risk.

In Florida?

It can be fully protected.

Important Caveat: The 1,215-Day Rule

If you haven’t lived in Florida long enough:

- Your homestead exemption may be capped under federal law

This is a critical detail that many people miss.

Personal Property Exemption

Florida offers a relatively modest personal property exemption.

Typical amount:

- $1,000 per person

Covers:

- Furniture

- Electronics

- Clothing

- Cash (to some extent)

The Wildcard (Sort Of)

Florida doesn’t have a traditional wildcard exemption—but it has something similar.

If you DO NOT claim a homestead:

You can use a $4,000 wildcard exemption.

This can be applied to:

- Cash

- Bank accounts

- Vehicles

- Any personal property

Why this matters:

If you don’t own a home (or don’t claim homestead), you get extra flexibility.

Motor Vehicle Exemption

Protection:

- $1,000 in vehicle equity

Example:

- Car value: $8,000

- Loan: $6,500

- Equity: $1,500

$1,000 is protected. The remaining $500 may need to be addressed.

Retirement Accounts (Very Strong Protection)

Good news:

Most retirement accounts are fully protected in Florida.

This includes:

- 401(k)s

- IRAs

- Pensions

- Profit-sharing plans

This is one of the strongest protections available.

Wages and Head of Household Protection

Florida has very strong wage protections, especially if you qualify as:

👉 Head of Household

If you provide more than half the support for a dependent:

- Wages may be fully exempt

- Especially if income is below certain thresholds

Even above those thresholds, additional protections may apply.

Public Benefits

These are fully protected:

- Social Security

- Disability benefits

- Unemployment

- Veterans benefits

These are considered essential income sources.

Life Insurance and Annuities (Florida Is VERY Generous Here)

Florida provides strong protection for:

- Life insurance proceeds

- Cash value of policies

- Annuities

This is another area where Florida stands out.

What Florida Does NOT Protect Well

Despite its strengths, Florida has some limitations:

❌ Low personal property exemption

❌ Limited vehicle exemption

❌ No traditional wildcard (unless no homestead)

This creates a trade-off:

Florida strongly protects big assets (like homes)…

but is weaker on smaller, flexible protections.

Chapter 7 vs. Chapter 13 in Florida

Chapter 7

- Exemptions determine what you keep

- Non-exempt assets could be liquidated

Chapter 13

- You keep everything

- You repay creditors based on non-exempt value

Exemptions still matter because they affect your payment plan.

Real-World Scenarios

Scenario 1: Homeowner with Equity

- $300,000 home equity

- Minimal other assets

Result:

Likely fully protected under Florida homestead exemption.

Scenario 2: Renter with Cash Savings

- $10,000 in savings

- No home

Result:

- $4,000 wildcard (if no homestead)

- Remaining amount may be exposed

Scenario 3: High-Income Head of Household

- Regular wages

- Supporting dependents

Result:

Wages may be fully protected.

Common Misconceptions About Florida Exemptions

❌ “I can keep everything no matter what.”

Not quite.

Florida protects certain assets extremely well—but not all assets.

❌ “My house is always protected.”

Only if:

- It qualifies as homestead

- You meet residency requirements

❌ “Cash is safe.”

Cash is often one of the least protected assets.

❌ “I don’t need to plan.”

This is a big mistake.

Exemption planning can dramatically affect your case.

Strategic Planning Matters (A Lot in Florida)

Because Florida’s system is uneven (very strong in some areas, weaker in others), planning is critical.

Before filing, people may:

- Time their filing

- Pay necessary expenses

- Allocate assets appropriately

Important:

This must always be done legally and transparently.

Never hide assets.

Why Florida Is Considered Debtor-Friendly

Florida is one of the most favorable states because of:

- Unlimited homestead protection

- Strong retirement protections

- Wage protections

- Insurance and annuity protections

These combine to create powerful outcomes for many filers.

The Emotional Reality

Most people considering bankruptcy are worried about one thing:

“Am I going to lose everything?”

In Florida, the answer is often:

“Probably not—and maybe less than you think.”

Understanding exemptions changes everything.

A Simple Way to Think About Florida Exemptions

If bankruptcy is the reset button…

Florida exemptions determine how much of your life stays intact when you press it.

Practical Tips for Florida Filers

1. Understand Your Home Status

Homestead is everything in Florida.

2. Don’t Ignore Cash

Cash is vulnerable without planning.

3. Know If You Qualify as Head of Household

This can dramatically protect your wages.

4. Be Honest

Full disclosure is always required.

5. Work With an Experienced Attorney

Florida exemption strategy is not DIY-friendly.

Final Thoughts: Florida Can Be Extremely Protective—If Used Correctly

Florida bankruptcy exemptions are among the most powerful in the country—but they require understanding and strategy.

So if you’re considering filing, remember:

- You must use Florida exemptions

- Your home may be fully protected

- Retirement and wages are strongly protected

- Planning makes a huge difference

And most importantly:

Bankruptcy in Florida isn’t about losing everything—it’s about protecting what matters most while moving forward.