(“Wait… California has TWO different exemption systems?”)

Yes—and choosing the right one can make or break your case.

If you’re filing bankruptcy in California, exemptions are not just important—they’re strategic. California gives you two completely different exemption systems, and picking the wrong one can cost you property you could have kept.

The good news? With the right understanding (and planning), California exemptions can be extremely powerful.

Let’s break it all down.

First: What Are Bankruptcy Exemptions?

At the most basic level:

Exemptions are laws that protect your property when you file bankruptcy.

Without them, creditors could potentially take everything you own.

With them, you get to keep:

- Essential property

- Basic necessities

- The foundation for a fresh start

Think of exemptions as a legal shield—they define what you walk away with after your case is over.

California Is an “Opt-Out” State—But With a Twist

California does NOT allow you to use federal exemptions.

Instead:

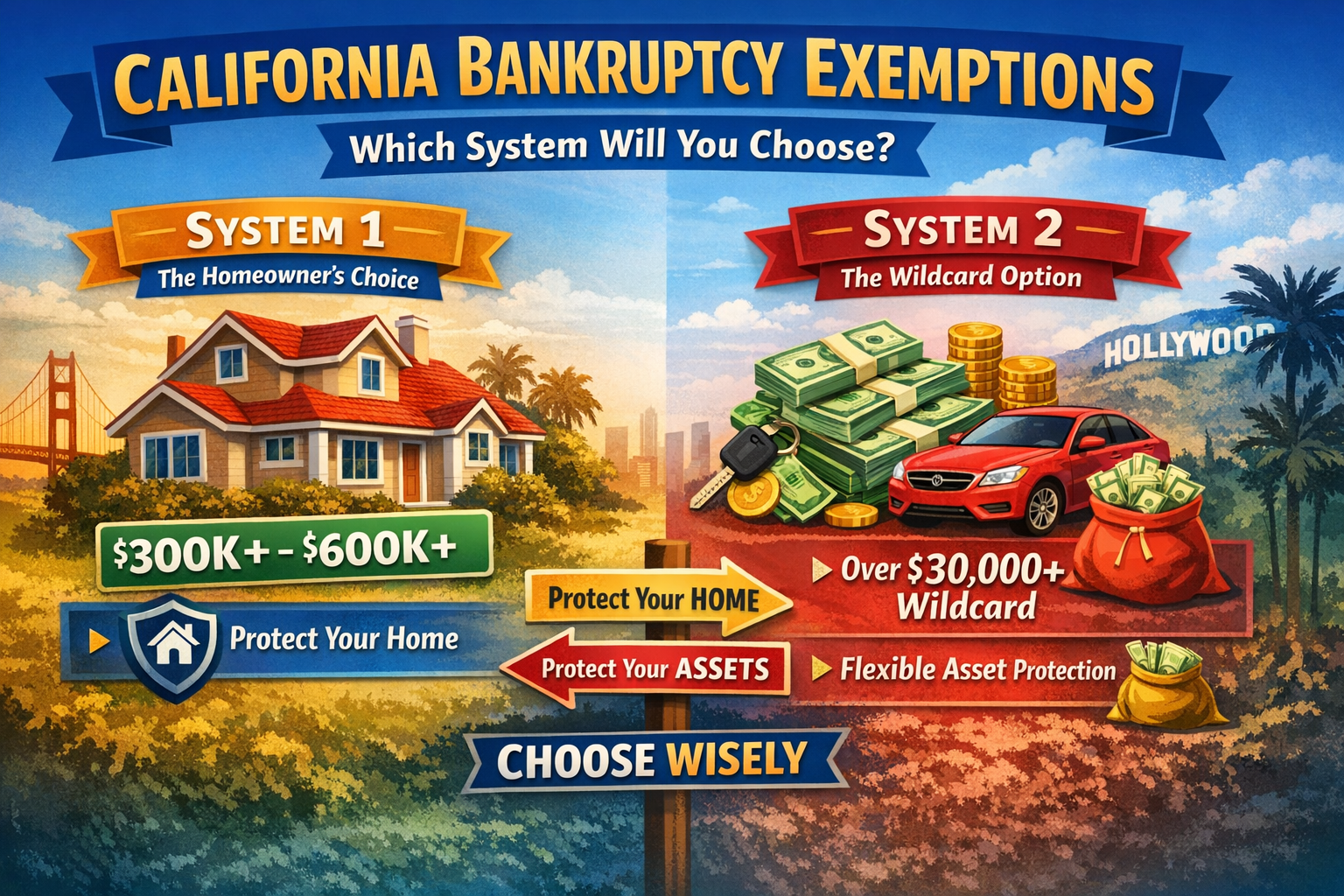

You must choose between two California exemption systems:

- System 1 (CCP §704)

- System 2 (CCP §703)

And you cannot mix and match.

The Big Question: Which System Should You Choose?

This is the most important decision in a California bankruptcy case.

👉 System 1 (704) is generally better if:

- You own a home

- You have significant home equity

👉 System 2 (703) is generally better if:

- You don’t own a home

- You have cash, savings, or miscellaneous assets

- You need flexibility (wildcard exemption)

Let’s break each one down.

System 1 (CCP §704): The “Homeowner-Friendly” System

This system is built around protecting your home.

1. Homestead Exemption (The Star of the Show)

California significantly expanded this exemption.

Protection:

- $300,000 to $600,000+ depending on county median home prices

This is one of the strongest homestead protections in the country.

Example:

- Home value: $800,000

- Mortgage: $400,000

- Equity: $400,000

In many cases:

That equity can be fully protected.

2. Motor Vehicle Exemption

Protection:

- Around $3,625 in vehicle equity

3. Household Goods

Covers:

- Furniture

- Appliances

- Clothing

These are typically protected because resale value is low.

4. Retirement Accounts

Fully protected in most cases

Includes:

- 401(k)s

- IRAs

- Pensions

5. Tools of the Trade

Protection:

- Around $8,725

Useful for:

- Contractors

- Skilled workers

6. Wages

California protects a portion of wages necessary for support.

The Limitation of System 1

Here’s the trade-off:

No wildcard exemption.

This means:

- Less flexibility

- Harder to protect cash or miscellaneous assets

System 2 (CCP §703): The “Wildcard Power” System

This is where things get interesting.

1. Wildcard Exemption (The MVP)

Protection:

- Over $30,000+ (combining unused homestead + wildcard)

This is one of the most powerful wildcard exemptions in the country.

What it can protect:

- Cash

- Bank accounts

- Vehicles

- Personal property

- Anything you choose

2. Homestead Exemption (Limited)

Protection:

- Around $31,575

Much smaller than System 1.

3. Motor Vehicle Exemption

Protection:

- Around $6,375

Better than System 1.

4. Personal Property

Covers:

- Household goods

- Clothing

- Electronics

5. Retirement Accounts

Still fully protected.

Why System 2 Is So Popular

Because of the wildcard.

Example:

You have:

- $15,000 in savings

- $5,000 car equity

- Personal property

Wildcard can protect all of it.

Real-World Comparison

Let’s say you have:

- $400,000 home equity

- $10,000 in savings

System 1:

- Home = protected

- Savings = exposed

System 2:

- Savings = protected

- Home = NOT fully protected

You must choose which matters more.

Chapter 7 vs. Chapter 13 in California

Chapter 7

- Exemptions determine what you keep

- Non-exempt assets may be liquidated

Chapter 13

- You keep everything

- You repay creditors based on non-exempt value

Exemptions still matter because they affect your payment plan.

Common Mistakes in California Cases

❌ Choosing the wrong system

This is the biggest mistake.

❌ Assuming “more exemptions = better”

It’s not about quantity—it’s about fit.

❌ Ignoring cash

Cash is often the most vulnerable asset.

❌ Not planning ahead

Timing and strategy matter.

Strategic Planning: Where California Gets Interesting

Because you have two systems, planning becomes critical.

Before filing, people may:

- Evaluate home equity

- Adjust timing

- Allocate exemptions strategically

Important:

This must always be done legally and transparently.

The Emotional Reality

Most people think:

“I’m going to lose everything.”

California exemptions often flip that to:

“I can actually keep most (or all) of what I have.”

Why California Can Be Extremely Powerful

Because it offers:

- Strong homestead protection (System 1)

- Massive wildcard flexibility (System 2)

- Strong retirement protections

- Strategic choice

Few states offer this level of flexibility.

A Simple Way to Think About It

If bankruptcy is the reset button…

California lets you choose which parts of your life you protect the most.

Practical Tips for California Filers

1. Know Your Equity

Especially in your home.

2. Evaluate Cash Carefully

Cash drives system choice.

3. Compare Both Systems

Never assume one is better.

4. Be Honest

Full disclosure is required.

5. Work With an Experienced Attorney

California exemption strategy is not DIY-friendly.

Final Thoughts: Choice Is Power

California bankruptcy exemptions are unique because they give you a choice—and that choice creates opportunity.

So if you’re considering filing, remember:

- You must choose between two systems

- One protects your home

- One protects everything else

- Strategy is everything

And most importantly:

Bankruptcy in California isn’t about losing everything—it’s about choosing what you protect and building your fresh start around it.