A wrong credit report can cost you real money—higher interest rates, denied housing, lost job opportunities, or higher insurance premiums.

The Fair Credit Reporting Act (FCRA) is designed to make credit reporting agencies and furnishers take accuracy seriously. Here’s what to know if your report is wrong.

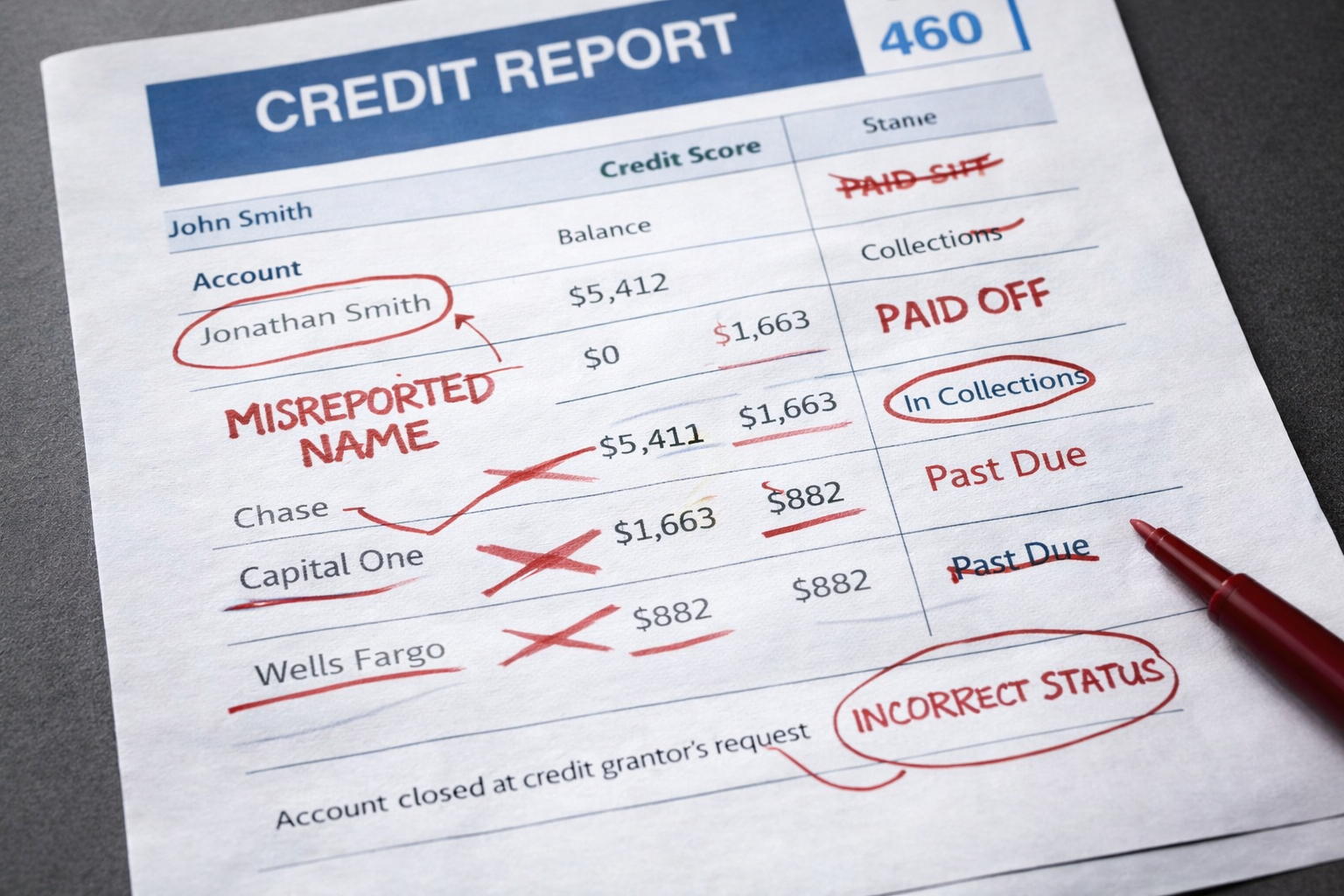

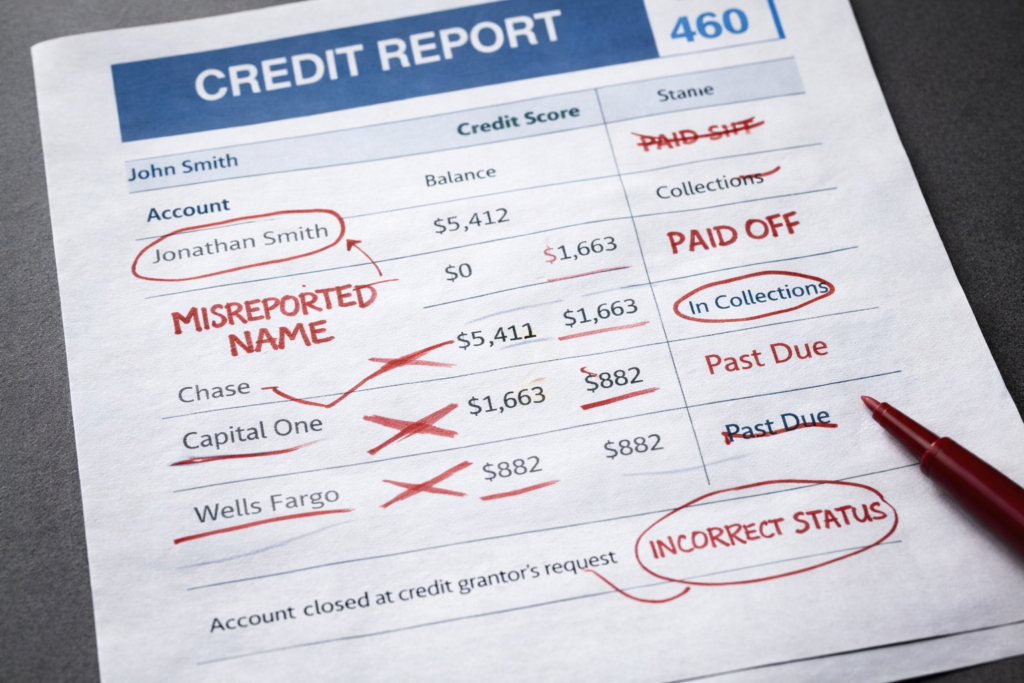

Common credit report errors

Some of the most common issues include:

- Accounts that aren’t yours

- Incorrect balances or payment history

- Duplicate accounts

- Wrong personal information (name, address, SSN fragments)

- Old debts that should have aged off

- Accounts marked “late” during disputes or hardships

Step 1: Pull your reports and identify the exact errors

Start by pulling your credit reports and highlighting:

- The account name

- The account number (partial)

- The specific inaccurate line item

- The date the error first appeared (if known)

Step 2: Dispute in writing (and keep proof)

Online disputes can be convenient, but written disputes create a cleaner paper trail.

Send disputes via certified mail when possible and keep:

- Copies of your dispute letters

- Proof of mailing

- The response letters

- Any updated reports

Step 3: Dispute with both the bureau and the furnisher

In many situations, you may need to dispute with:

- The credit reporting agency (Experian, Equifax, TransUnion)

- The company furnishing the information (creditor/collector)

Step 4: Don’t send originals

Send copies of supporting documents, not originals.

Step 5: Track timelines and outcomes

Write down:

- When you sent the dispute

- When you received responses

- What changed (or didn’t)

Bottom line

Credit reporting errors are not just annoying—they can be financially damaging. If you’ve disputed and the information remains wrong, it may be time to get legal advice.

If your credit report is inaccurate and disputes aren’t fixing it, Ginsburg Law Group can help you understand your options under the FCRA.