Is It Still Necessary with Portability?

For years, married couples with significant wealth used A/B trust planning (also called a credit shelter trust or bypass trust strategy) to reduce federal estate taxes.

But today, with the federal estate tax exemption at historically high levels — and portability available — many Arizona couples ask:

“Do we still need an A/B trust if our estate is around $30 million?”

The answer depends on more than just today’s exemption amount.

Let’s break it down.

The Current Federal Estate Tax Landscape

As of now:

- The federal estate tax exemption is over $13 million per person

- A married couple can effectively shield over $27 million with portability

- The federal estate tax rate is 40% on amounts above the exemption

However:

- The higher exemption is scheduled to sunset in 2026

- It could drop roughly in half (unless Congress acts)

For a $30 million Arizona couple, that sunset matters.

What Is A/B Trust Planning?

Under traditional A/B trust planning:

When the first spouse dies:

- An amount equal to their estate tax exemption funds the B Trust (Bypass/Credit Shelter Trust)

- The remaining assets pass to the A Trust (Marital Trust) for the surviving spouse

The B Trust:

- Is not included in the surviving spouse’s estate

- Can benefit the surviving spouse

- Passes tax-free to children at the second death

This structure “locks in” the first spouse’s exemption.

What Is Portability?

Portability allows the surviving spouse to inherit the unused exemption of the first spouse to die — if a timely estate tax return is filed.

In theory, portability makes A/B planning unnecessary for many couples.

But portability is not identical to a credit shelter trust.

Key Considerations for a $30 Million Arizona Estate

1. Sunset Risk

If the exemption drops to approximately $6–7 million per person in 2026:

- A married couple may only shield around $12–14 million combined

- A $30 million estate could face estate tax on $16–18 million

- At 40%, that could mean $6–7+ million in federal estate tax

An A/B trust locks in the exemption of the first spouse at death — even if the law changes later.

2. Asset Growth

Portability does not shelter post-death appreciation.

Example:

- First spouse dies with $13 million exemption unused.

- Surviving spouse inherits and assets grow significantly.

- Growth above exemption may be taxable.

With a Bypass Trust:

- Appreciation on B Trust assets stays outside the surviving spouse’s estate.

For high-growth portfolios, this is critical.

3. Arizona Has No State Estate Tax

Arizona does not impose a state estate tax.

That simplifies planning — federal tax is the primary concern.

However, federal tax exposure at $30 million is still significant.

4. Asset Protection Benefits

A Bypass Trust can:

- Protect assets from surviving spouse’s creditors

- Provide remarriage protection

- Ensure children from a prior marriage are protected

- Prevent unintended disinheritance

Portability offers no asset protection.

5. Step-Up in Basis Considerations

One tradeoff:

- Assets in the surviving spouse’s estate receive a second step-up in basis at death.

- Bypass Trust assets do not receive a second step-up.

For highly appreciated assets, this income tax issue must be weighed against estate tax savings.

At $30 million, estate tax exposure often outweighs capital gains concerns — but modeling is essential.

When Portability Alone May Be Enough

Portability may suffice if:

- Combined estate will remain under post-sunset exemption levels

- No remarriage concerns

- No asset protection concerns

- Minimal growth expected

- Family situation is straightforward

For estates near $30 million, portability alone can be risky if laws change.

A Modern Hybrid Approach

Today, many Arizona estate plans use flexible structures such as:

- Disclaimer-based A/B trusts

- Clayton elections

- Formula clauses tied to exemption amounts

This allows post-death tax planning flexibility based on:

- Law in effect at death

- Asset values

- Family circumstances

Flexibility is often more valuable than rigid structures.

Example: $30 Million Arizona Couple

Assume:

- $30 million total estate

- Exemption drops to ~$7 million per spouse

- Estate grows to $35 million by second death

Without A/B planning:

- Large portion may be exposed to 40% tax

With properly structured bypass planning:

- First spouse’s exemption locked in

- Appreciation on B Trust sheltered

- Potential multi-million dollar tax savings

So — Is A/B Planning Still Relevant?

For Arizona couples with $30 million:

Yes, it absolutely can be.

Even with portability, A/B trust planning may:

- Hedge against exemption reduction

- Protect appreciation

- Provide creditor and remarriage protection

- Preserve wealth for children

The key is designing the right structure — not blindly using old templates.

The Bottom Line

At $30 million, estate tax exposure is real — especially after 2026.

Portability helps, but it is not a complete substitute for credit shelter planning.

Modern estate planning should include:

- Federal estate tax modeling

- Growth projections

- Basis step-up analysis

- Asset protection review

- Flexible drafting

For high-net-worth Arizona families, thoughtful A/B trust planning remains a powerful tool.

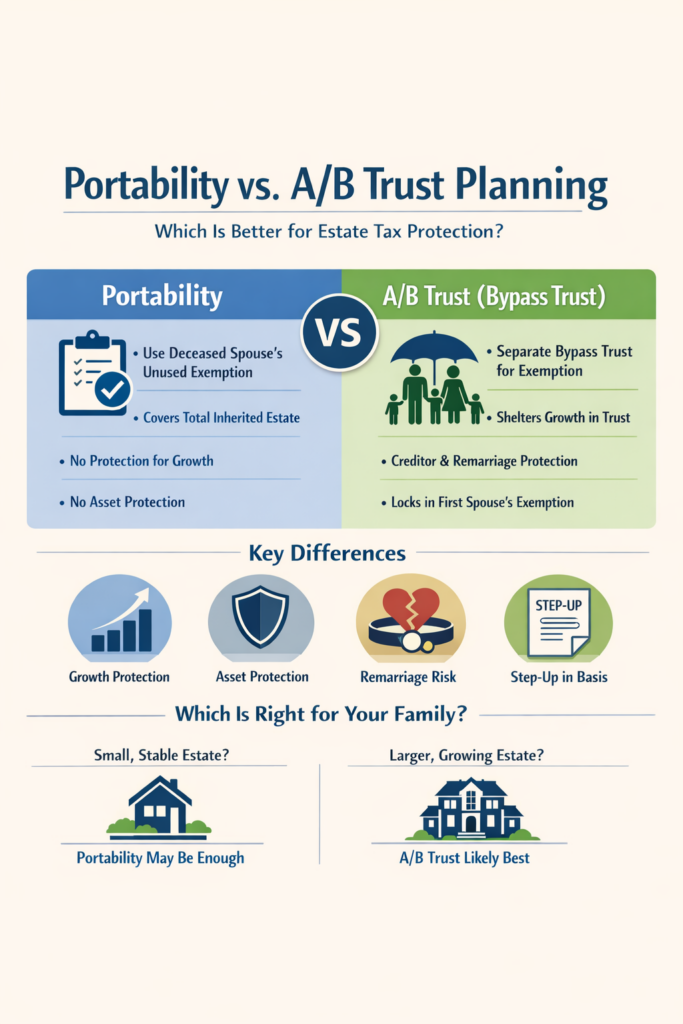

Portability vs. A/B Trust Planning

Which Is Better for Estate Tax Protection?

Married couples with significant assets often ask:

“Do we still need an A/B trust, or is portability enough?”

Both strategies are designed to preserve each spouse’s federal estate tax exemption — but they work differently and offer different benefits.

Here’s how they compare.

Quick Overview

- Portability allows a surviving spouse to “inherit” the unused estate tax exemption of the first spouse to die.

- A/B Trust Planning (Credit Shelter or Bypass Trust planning) uses a trust structure to lock in the first spouse’s exemption and remove assets from the surviving spouse’s taxable estate.

They are not identical.

Side-by-Side Comparison

| Issue | Portability | A/B Trust (Bypass Trust) |

|---|---|---|

| How It Works | Surviving spouse elects to use deceased spouse’s unused exemption by filing an estate tax return. | First spouse’s exemption funds a Bypass Trust at death; assets remain outside surviving spouse’s estate. |

| Locks in First Spouse’s Exemption? | Yes, if properly elected. | Yes, automatically via trust funding. |

| Protects Post-Death Appreciation? | No — future growth is included in surviving spouse’s estate. | Yes — growth inside Bypass Trust is excluded from survivor’s estate. |

| Asset Protection | No built-in protection. | Can protect from creditors, remarriage risks, and future disputes. |

| Remarriage Risk | Portability can be lost if surviving spouse remarries and new spouse dies first. | Not affected by remarriage. |

| Step-Up in Basis at Second Death | Yes — assets included in surviving spouse’s estate receive full step-up. | No second step-up on Bypass Trust assets (unless special planning included). |

| Administrative Complexity | Simpler; requires timely estate tax return filing. | More complex; ongoing trust administration required. |

| Flexibility After First Death | Limited once election is made. | Can be structured with flexibility (disclaimer or formula planning). |

| Best For | Moderate estates unlikely to exceed exemption even after growth. | Larger estates or families needing tax and asset protection planning. |

The Big Differences

1. Appreciation Matters

Portability does not shelter growth after the first spouse’s death.

If:

- Estate is $25 million at first death

- Surviving spouse lives 15 more years

- Assets grow significantly

All growth is taxed at the second death.

With a Bypass Trust:

- The first spouse’s funded portion — and its appreciation — stay outside the taxable estate.

For high-growth portfolios, this can mean millions in tax savings.

2. Asset Protection

Portability provides no protection from:

- Creditors

- Lawsuits

- Remarriage complications

- Changes in estate plan by surviving spouse

A properly drafted Bypass Trust can:

- Preserve assets for children

- Protect from creditors

- Guard against disinheritance in second marriages

3. Income Tax Tradeoff

One advantage of portability:

Assets included in the surviving spouse’s estate receive a second step-up in basis, potentially reducing capital gains tax for heirs.

Bypass Trust assets typically do not receive that second step-up (unless specially structured).

For some families, this income tax benefit may outweigh estate tax savings — modeling is essential.

When Portability May Be Enough

Portability may be sufficient if:

- Combined estate is well below projected exemption levels

- Minimal asset growth expected

- No remarriage concerns

- No asset protection concerns

- Family structure is simple

When an A/B Trust May Be Preferable

A/B planning often makes sense if:

- Estate is $20–30+ million

- Significant appreciation expected

- Exemption reduction (sunset risk) is a concern

- Asset protection is important

- There are blended family dynamics

- Long-term wealth preservation is a priority

Modern Planning: It’s Not All or Nothing

Today, many estate plans use flexible tools like:

- Disclaimer A/B trusts

- Clayton elections

- Formula funding clauses

This allows decisions to be made after the first death based on:

- Asset values

- Tax law in effect

- Family circumstances

Flexibility is often more valuable than rigid structures.

The Bottom Line

Portability is simpler.

A/B trust planning is more protective.

For larger estates, especially those approaching or exceeding projected exemption levels, A/B planning can provide:

- Appreciation protection

- Asset protection

- Remarriage protection

- Long-term tax efficiency

The right answer depends on estate size, growth expectations, family dynamics, and tax projections.

Thoughtful modeling — not guesswork — should drive the decision.